Advanced Micro Devices Inc - DCF model

Today I am delighted to present to my esteemed followers $AMD DCF valuation model.

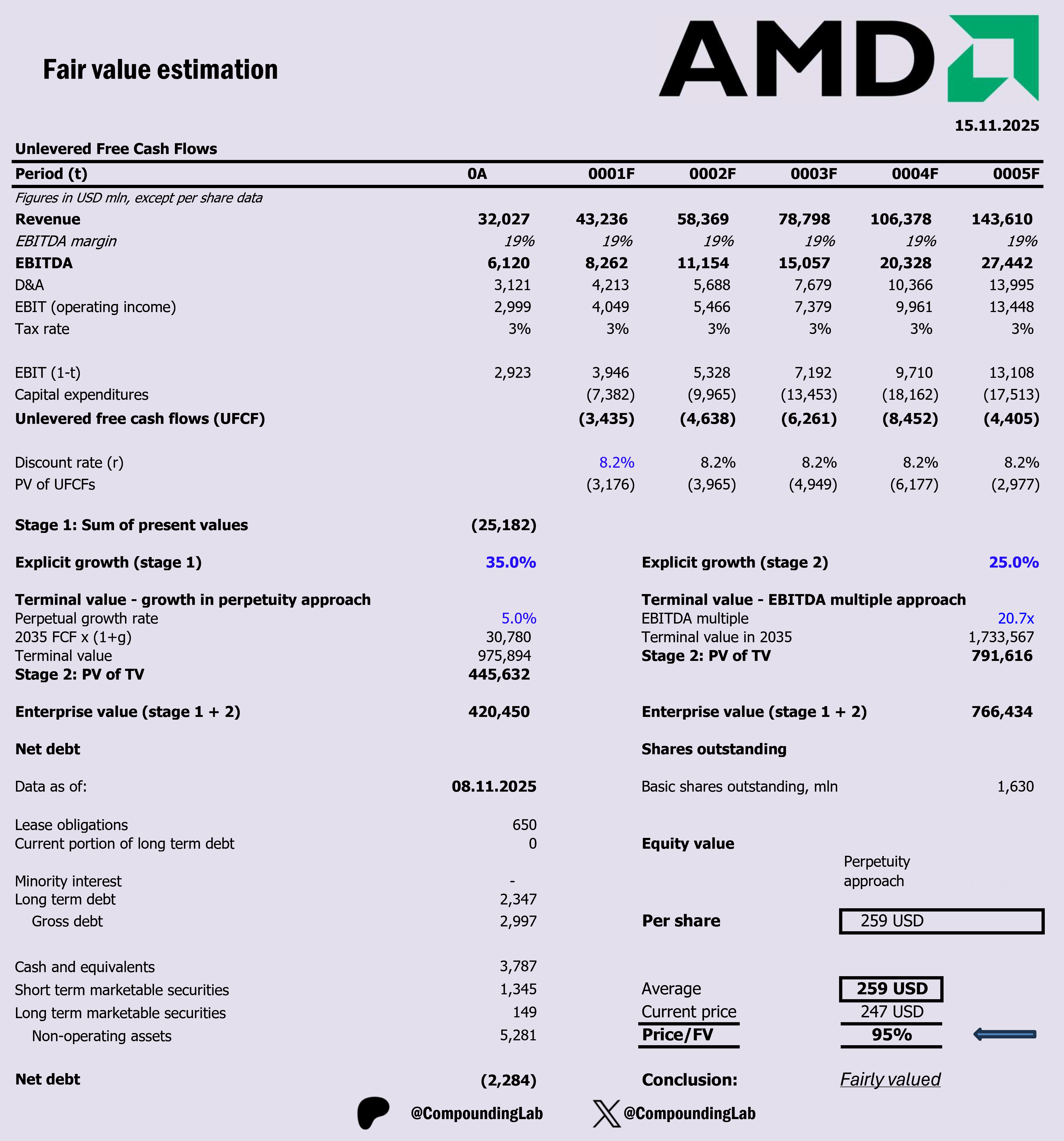

Valuation suggests that the stock is trading at fair value. I am not sharing here AMD’s history or recent announcement – all this is available online. But I do want to stress out that evaluating this stock is quite a challenging exercise, therefore, I encourage you to consider my model with a degree of a reasonable skepticism.

Key assumptions:

1. Explicit 5Y growth @ 35% and slightly lower for the second 5Y period (https://ir.amd.com/news-events/press-releases/detail/1266/amd-unveils-strategy-to-lead-the-1-trillion-compute-market-and-accelerate-next-phase-of-growth)

2. Long-term growth in perpetuity @ 5%

3. WACC @ 8.2%

4. An EBITDA exit multiple of 20.7 (http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/vebitda.html).

Unfortunately, the EV/EBITDA approach yields a value that is unreasonably high, so I have excluded it from this analysis and am presenting only the FCFF-based valuation for prudence.

5. Reinvestment: The input that drives reinvestment is the most recent Sales to Capital ratio = 2.05