$AMZN valuation model

A framework for estimating AMZN intrinsic value using forward cash flow expectations and long-term operating assumptions.

$AMZN valuation model ready for your review, subs.

You wouldn’t want Amazon to enter your industry. They can disrupt almost any moat really quickly. There is a phenomenon often called the “Amazon effect” - when Amazon enters a market, incumbents often see margins compress, valuations fall, and customer expectations reset very quickly. That said, Amazon is not universally unbeatable. Their success depends heavily on whether the industry matches Amazon’s core strengths. Let’s check what is under the hood.

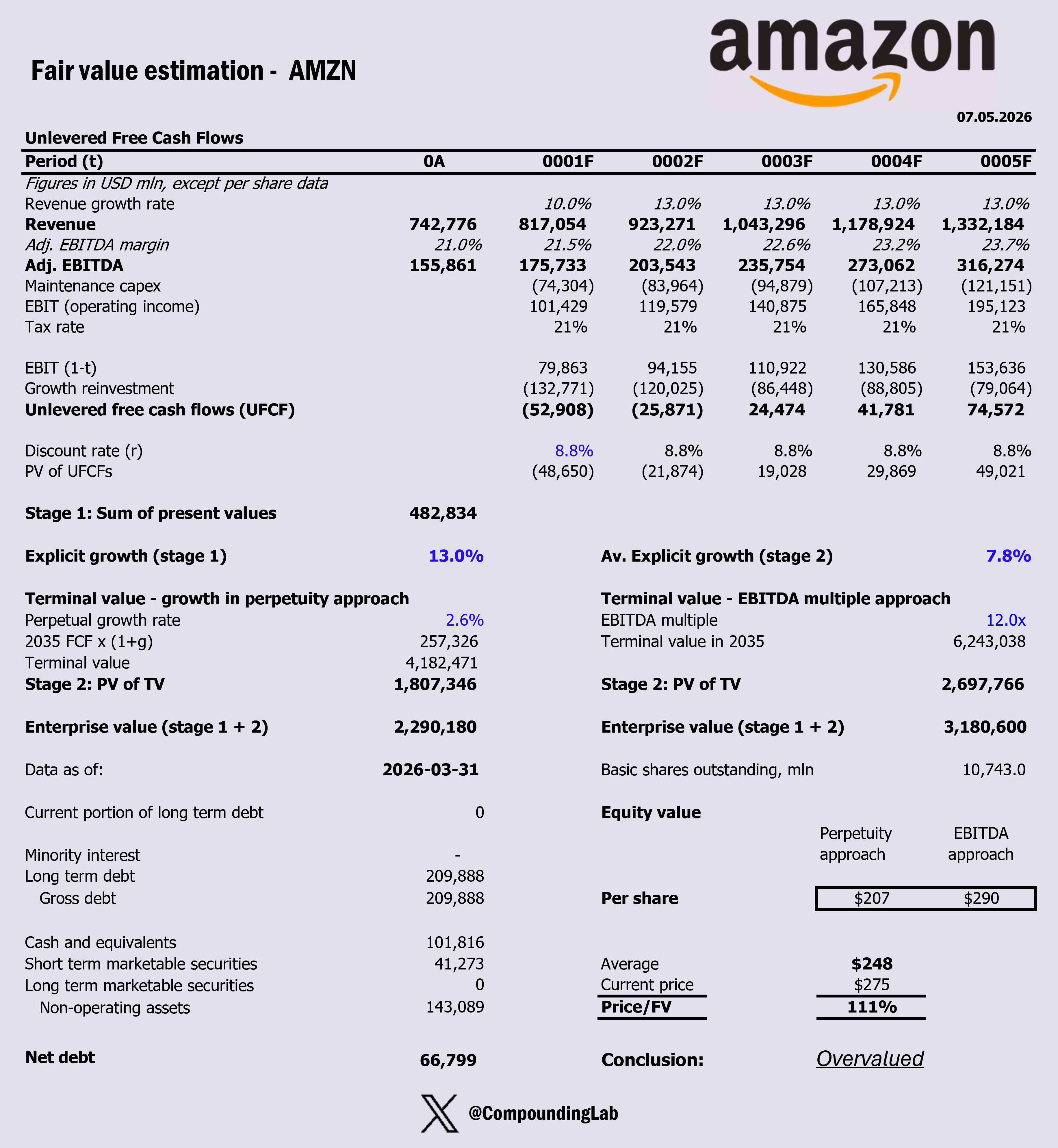

Key assumptions:

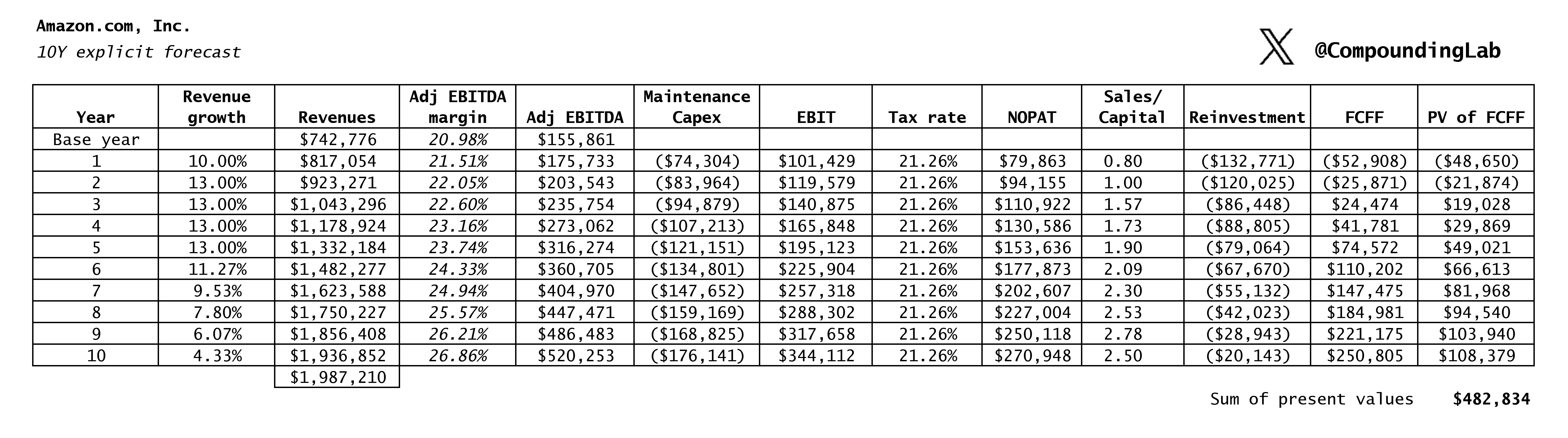

Explicit average 5Y/5Y growth @ 13%/7.8%

Long-term growth in perpetuity @ 2.6%

Adj. EBITDA Margin expansion from 21% to 27% in Y10

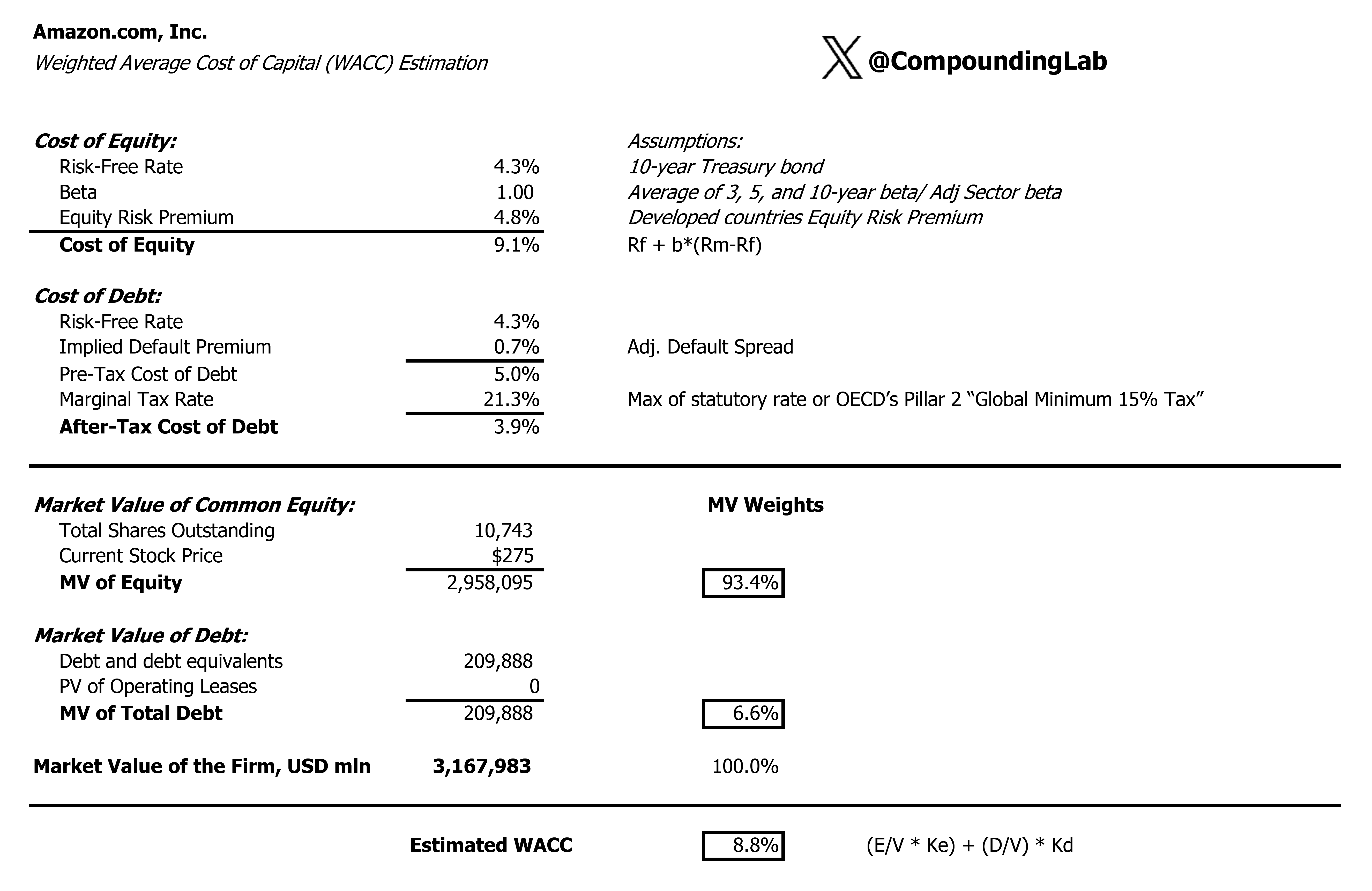

WACC @ 8.8%

Adj. EBITDA exit multiple of 12

Marginal tax rate 21%

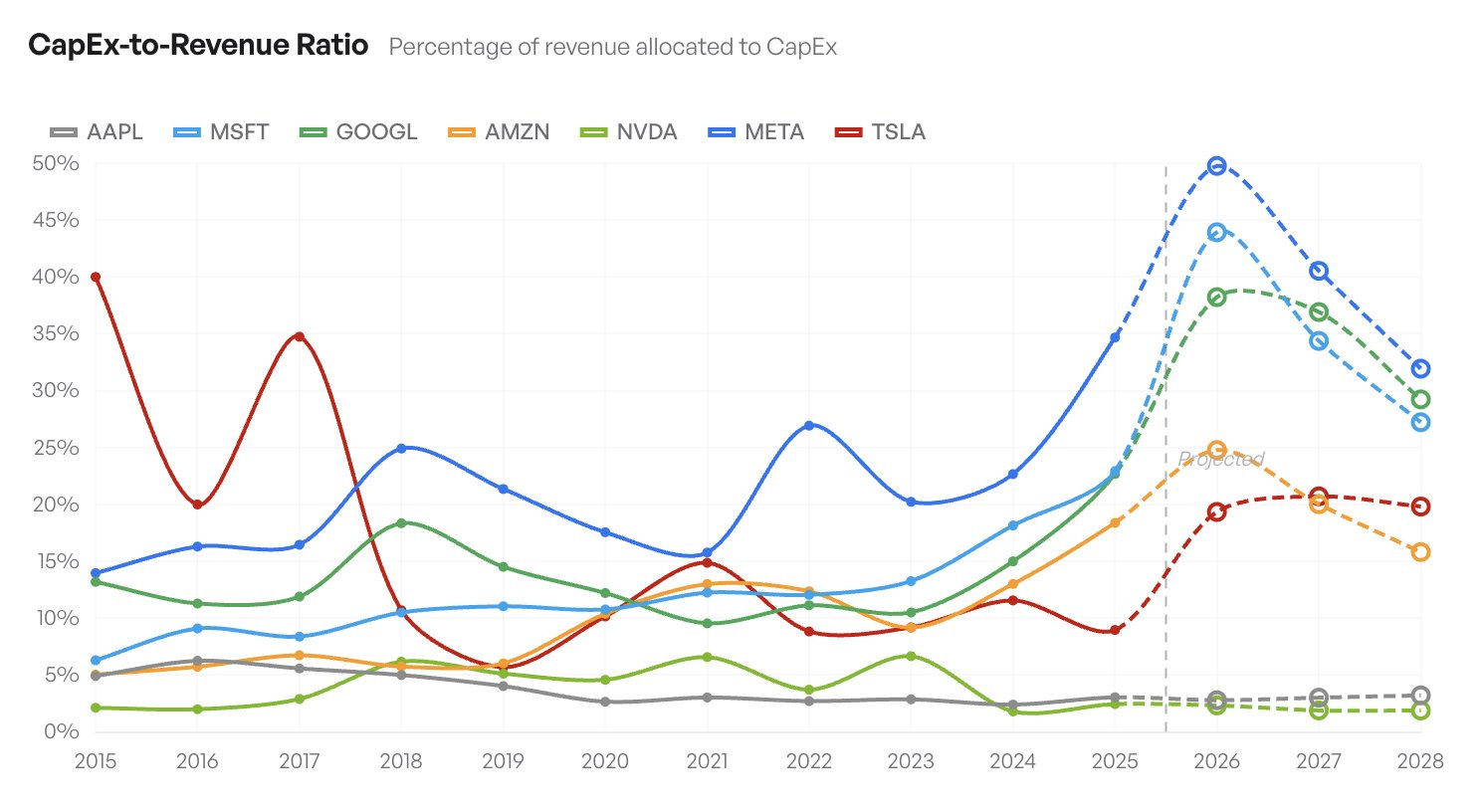

The input that drives reinvestment is Sales/Capital ratio, gradually increasing from 0.8 in 2026 (due to heavy capex) to 2.5 in year 10

Historic Growth (for context)

Amazon’s journey is truly inspiring. Starting from a humble garage-based startup selling books online in 1994, it has transformed into a vast marketplace that has truly reshaped both retail and technology. Jeff Bezos took the company public in 1997 with only $148 million in revenue. Despite challenges like the dot-com bust, Amazon kept its focus on customers, launching Prime in 2005 and AWS in 2006, which fueled its growth into a profit-making powerhouse. The company’s steady management and visionary approach have been key. In 2025, Amazon’s revenue reached $717 billion, growing steadily in the low teens, which is a bit below its impressive 10-year CAGR of 21%.

We know that it is difficult to sustain growth. And Amazon is a vivid example. Consensus estimates currently imply that Amazon will grow revenue at roughly 11-13% CAGR over the next 5 years, with the near-term years expected around low-to-mid teens growth.

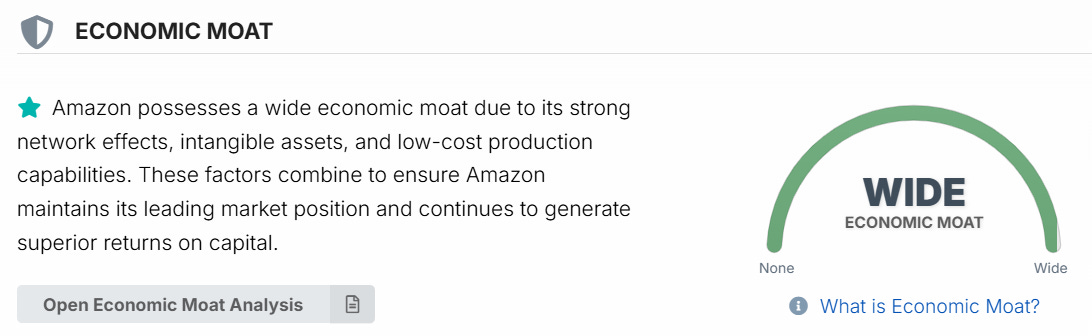

Moat

Amazon has a Wide moat and exemplary capital allocation.

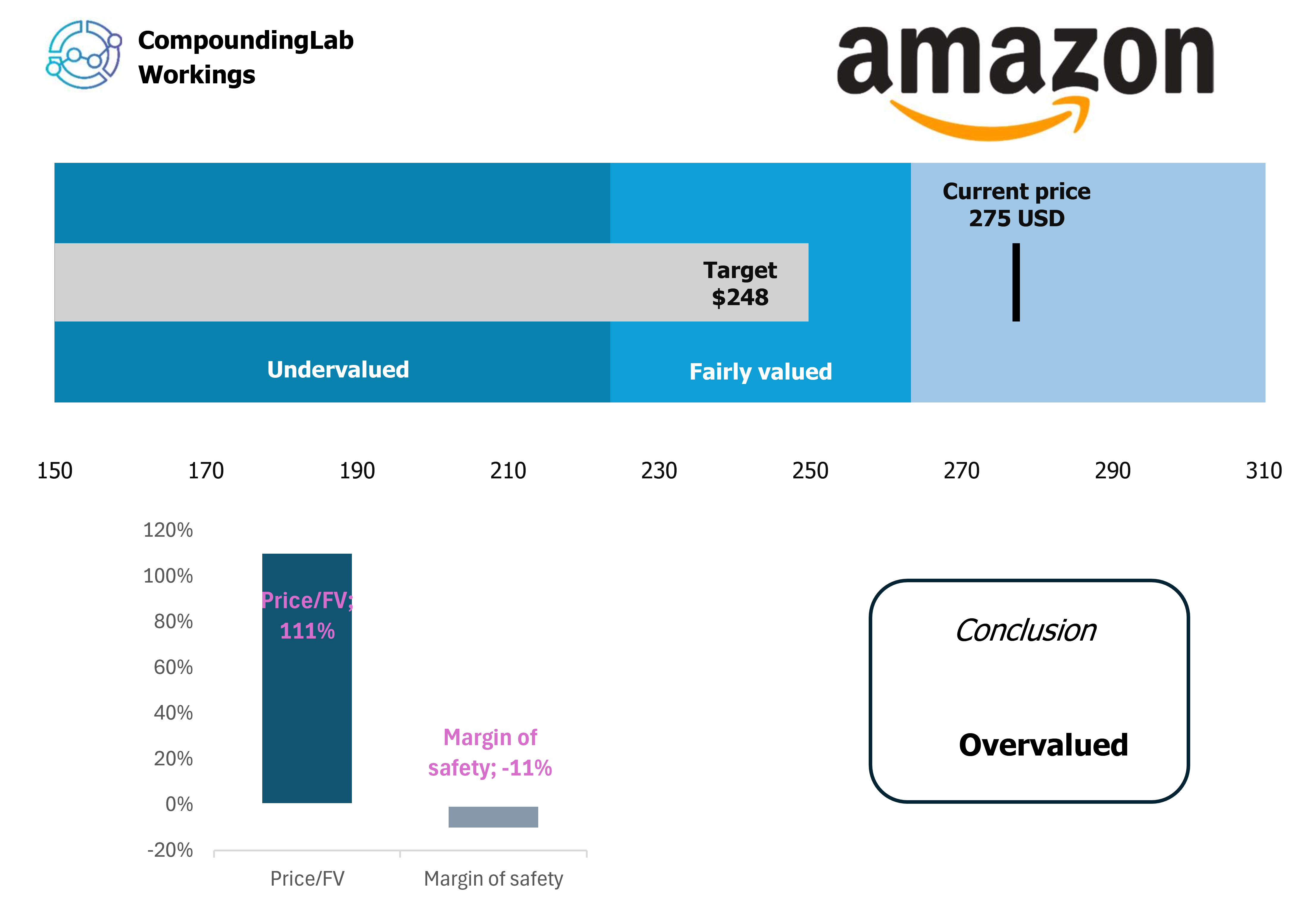

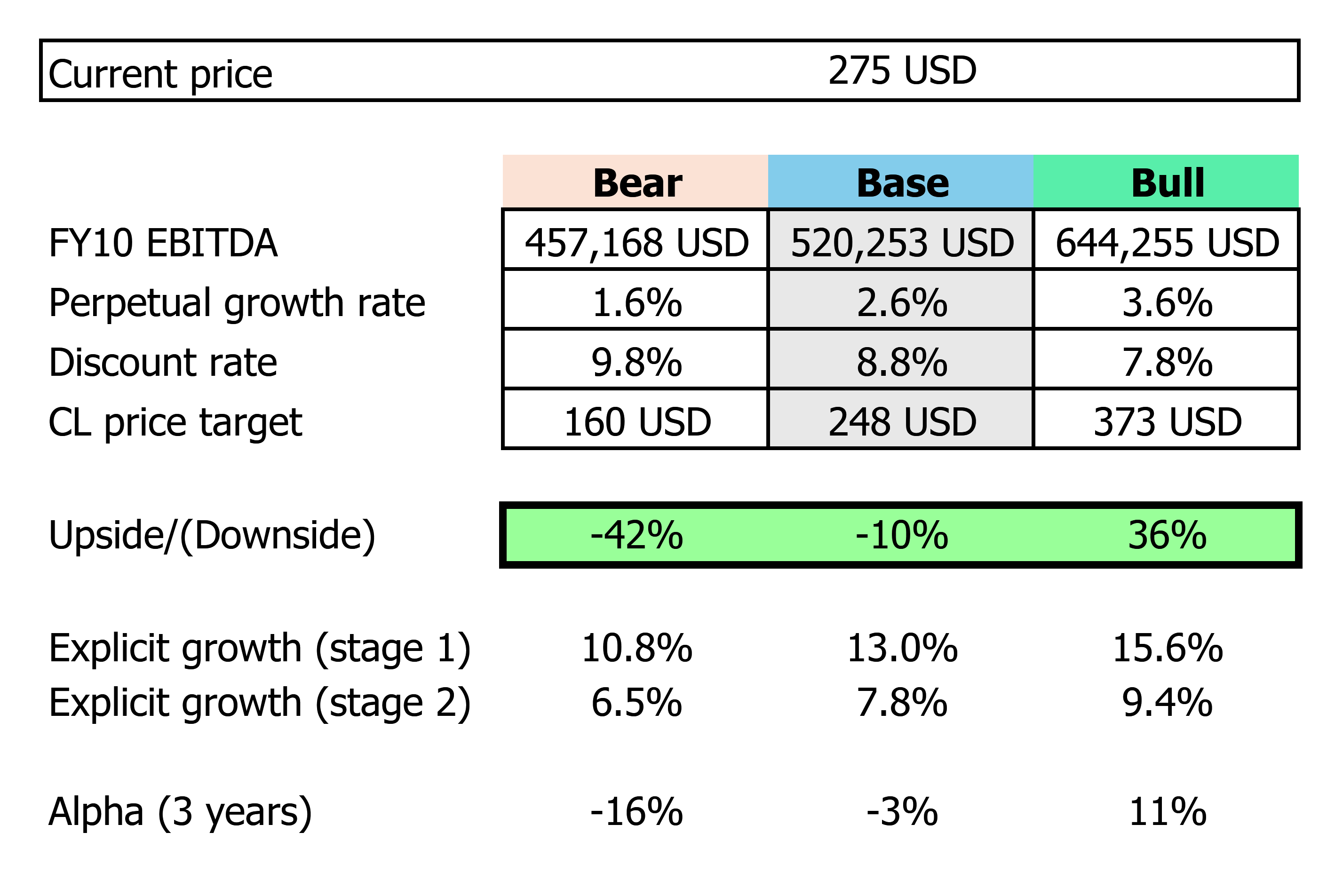

Base case

CL price target for Amazon is 248. Valuation suggests that the stock is trading at 11% premium to fair value. If adjusted to FV within 3 years, it will generate -3% in annual underperformance.

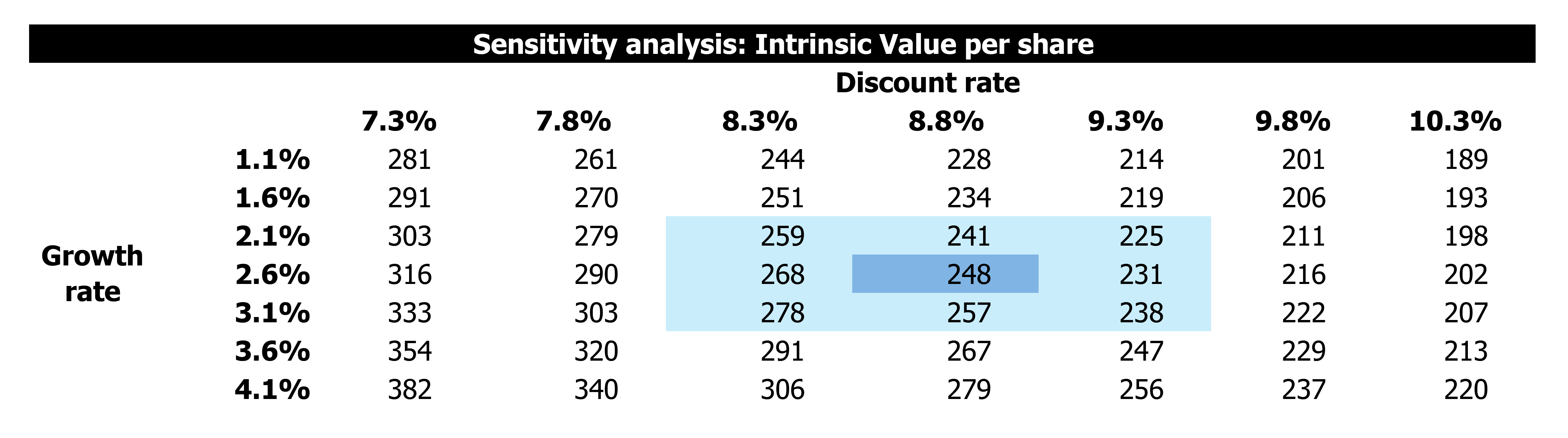

Sensitivity

If you disagree on certain aspects, you can choose your own assumptions based on the tables below.

Also, feel free to share this article by pressing the button below so that more people can see it.

Base case + Bear case + Bull case:

Sensitivity table:

Conclusion

Amazon is a wonderful company trading at a premium to intrinsic value.

________________________________

Disclaimer: This post is for informational and educational purposes only. I do not own shares in AMZN but can buy/sell them at any time after this post is published. Not financial advice. Do your own research.