$DHI

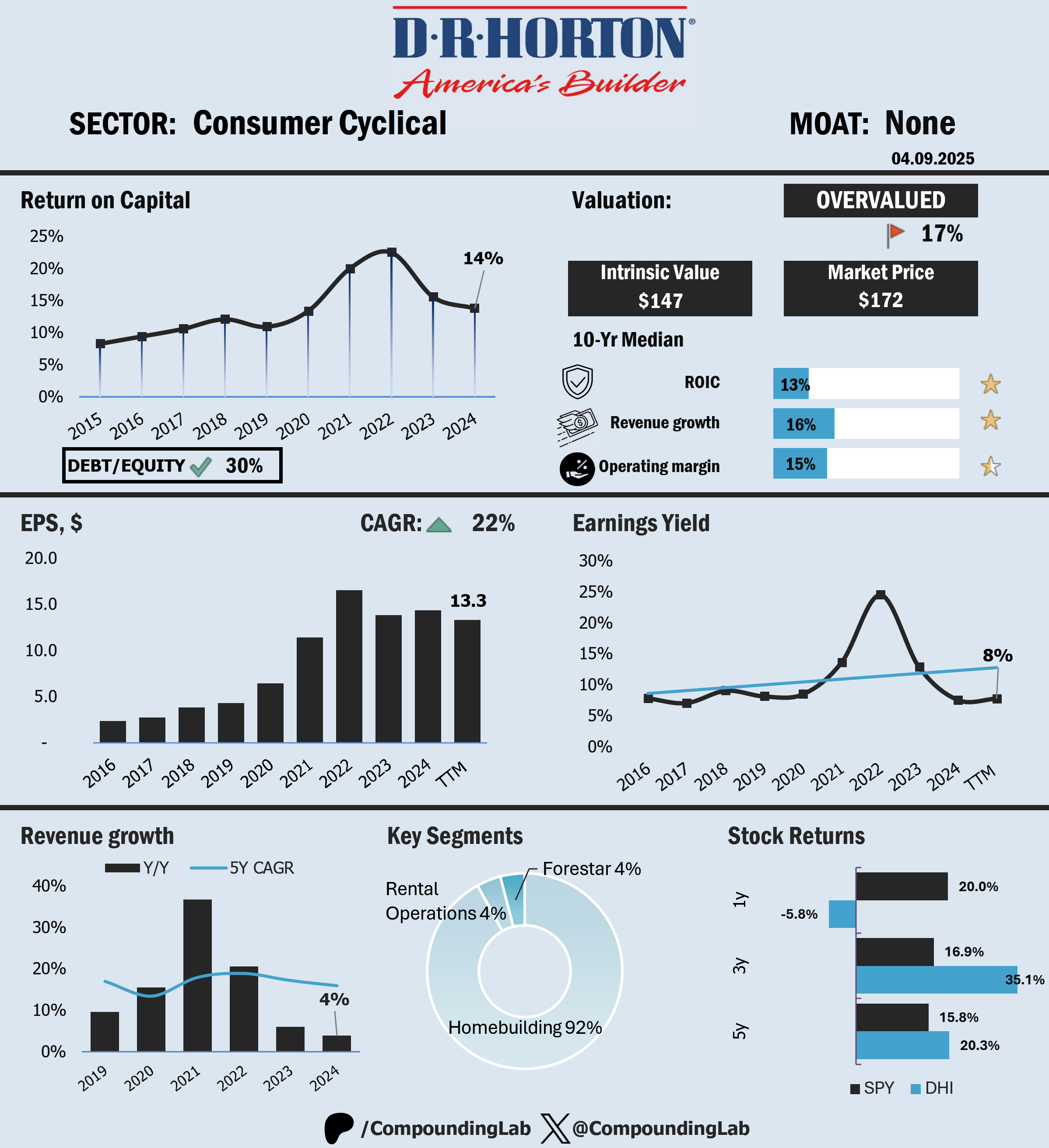

D.R. Horton is riding high in the homebuilding sector, but it seems that its stock price is running ahead of fundamentals.

ROIC and growth are decent, which is evidenced in high 3Y and 5Y stock return, but in the most recent year stock was down 6%, reflecting challenging conditions for the US housing market. Many borrowers are eagerly anticipating a cut in the key interest rate, hoping it will finally bring them some relief.

From a moat perspective, homebuilders are rarely assigned with any moat due to very cyclical, competitive, and capital-intensive industry.

2022 peak in earnings yield indicates a very attractive point for entry was in 2022, when D.R. Horton was trading at 70$. Since then, stock delivered 35% shareholders' return every year.

Currently at 176$, shares are trading at a premium to fair value; therefore, I do not see shares as attractive. Disposal of DHI will be a reasonable move, despite the expected rate cut.

Feel free to share your take - would you buy, hold, or sell DHI at today’s levels?

You can also leave a comment if you’d like OnePager for your selected ticker.