$GPN

Get a cup of coffee.

In this post, I’ll walk you through $GPN fundamentals.

Billions in goodwill. A maze of deals. And now the market smells something. Is this a broken roll-up or the setup for the most misunderstood rebound in payments? 👀

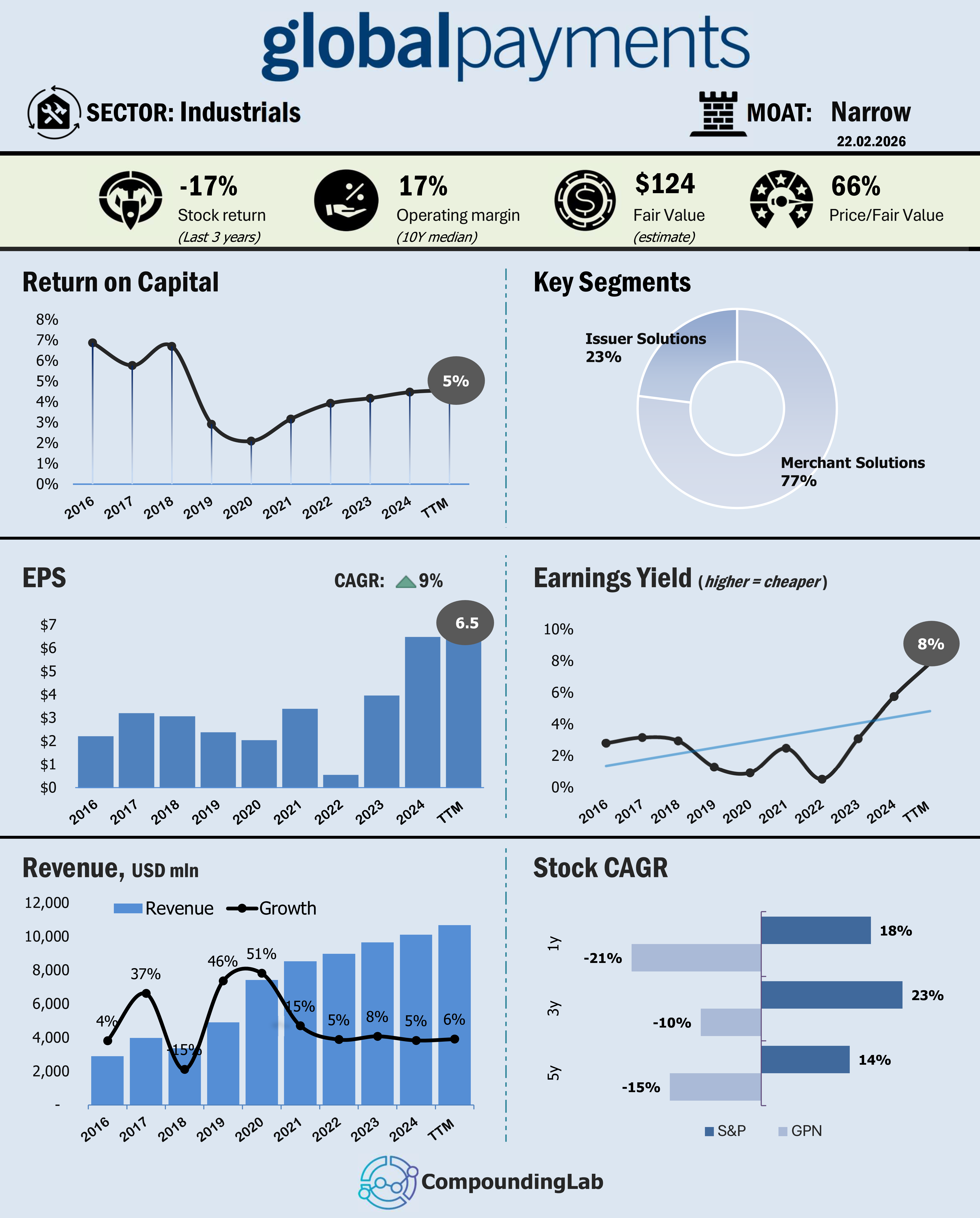

Years of aggressive acquisitions have left the story tangled in goodwill, leverage, and integration noise. Since the transformational merger with Total System Services and subsequent deals like EVO Payments, reported fundamentals have become harder to read at a glance. But beneath the accounting fog sits a scaled global processor generating resilient cash flows across merchant and issuer solutions. To see whether Global Payments is a value trap or a mispriced compounder, we need to strip the narrative away and let the fundamentals speak.

Over the past 12 months, Global Payments has materially underperformed the S&P 500, and the gap widens as you extend the timeframe. While the index continues to grind higher on mega-cap strength and AI-driven optimism, GPN remains stuck well below prior cycle highs. This is not a one-quarter anomaly - it is persistent relative weakness across 1Y, 3Y, and 5Y periods.

The reason for the lag is not mysterious. Investors are discounting integration fatigue, elevated leverage, and skepticism around capital allocation after years of acquisition/merger-led growth. Payments as a sector has not collapsed - peers with cleaner balance sheets and simpler stories have held up far better (exclude Paypal). The market is applying a “prove it” discount to GPN.

From a capital efficiency standpoint, the long-term picture is mixed. The 10-year median ROIC of ~5% is uninspiring for a scaled payments platform. In an industry where high-single to low-double-digit ROIC is achievable for best-in-class operators, GPN’s returns suggest that acquisition premiums and integration costs have diluted economic performance. The 2019 merger with Total System Services (TSYS) was transformational in scale - but not in returns. GPN issued a significant amount of equity to fund the deal, expanding the asset base while post-merger ROIC remained compressed. Share count rose, goodwill ballooned, and per-share value creation stalled. That is the core reason long-term shareholders have been disappointed.

Leverage adds another layer. With a Debt/Equity ratio near 80%, the balance sheet is not distressed, but it limits flexibility. Historically, markets reward simplicity and low leverage. GPN offers neither.

At the current price of $82, the stock trades at an earnings yield of ~8%. Decomposed, that yield reflects three elements: a risk premium for leverage and acquisition history, muted confidence in sustainable growth, and concern about return quality. If management stabilizes ROIC and restrains capital allocation, that yield could compress materially.

Competitive positioning remains solid. GPN likely qualifies as a narrow moat business, derived primarily from switching costs, scale advantages in merchant acquiring, and deep integrations across software ecosystems. Payments infrastructure is sticky. Once embedded, it is rarely replaced casually.

Historically, revenue growth has averaged roughly 15%, largely acquisition-driven. Organic growth has been mid-single digits - respectable but not industry-leading. Compared to faster-growing fintech-native competitors, GPN is more mature and diversified, with meaningful exposure across Merchant Solutions (largest segment) and Issuer Solutions. Market share in global merchant acquiring is meaningful but not dominant; this is a scale player, not a monopoly.

Operating margin around 17% is acceptable but not best-in-class. Industry leaders sometimes exceed 20%+. This suggests operational competence, but not structural superiority.

Drawdowns have been severe. The stock has experienced multiple 40–60% peak-to-trough declines (currently in 62%) over the past decade, reflecting leverage, integration risk, and sentiment cyclicality.

Assuming prudent management, no further value-destructive acquisitions, and gradual normalization of ROIC, intrinsic value estimates cluster around $124 per share, implying roughly 34% upside from $82. The valuation already embeds skepticism. The question is simple: will management start compounding or repeat history?

_______________________________________________

Disclaimer: This post is for informational and educational purposes only. I do not own shares in GPN but can buy/sell at any time after this post is published. Not financial advice. Do your own research.

Interesting breakdown of GPN beneath the acquisition fog. I like how you separate narrative from fundamentals and frame this as a ROIC and capital allocation story rather than just a valuation call. At these levels it really feels like a “prove it” setup. What would be the key signal for you that management has truly shifted toward compounding instead of deal-making?

I’ve subscribed and would be happy to support each other.

Jorrit