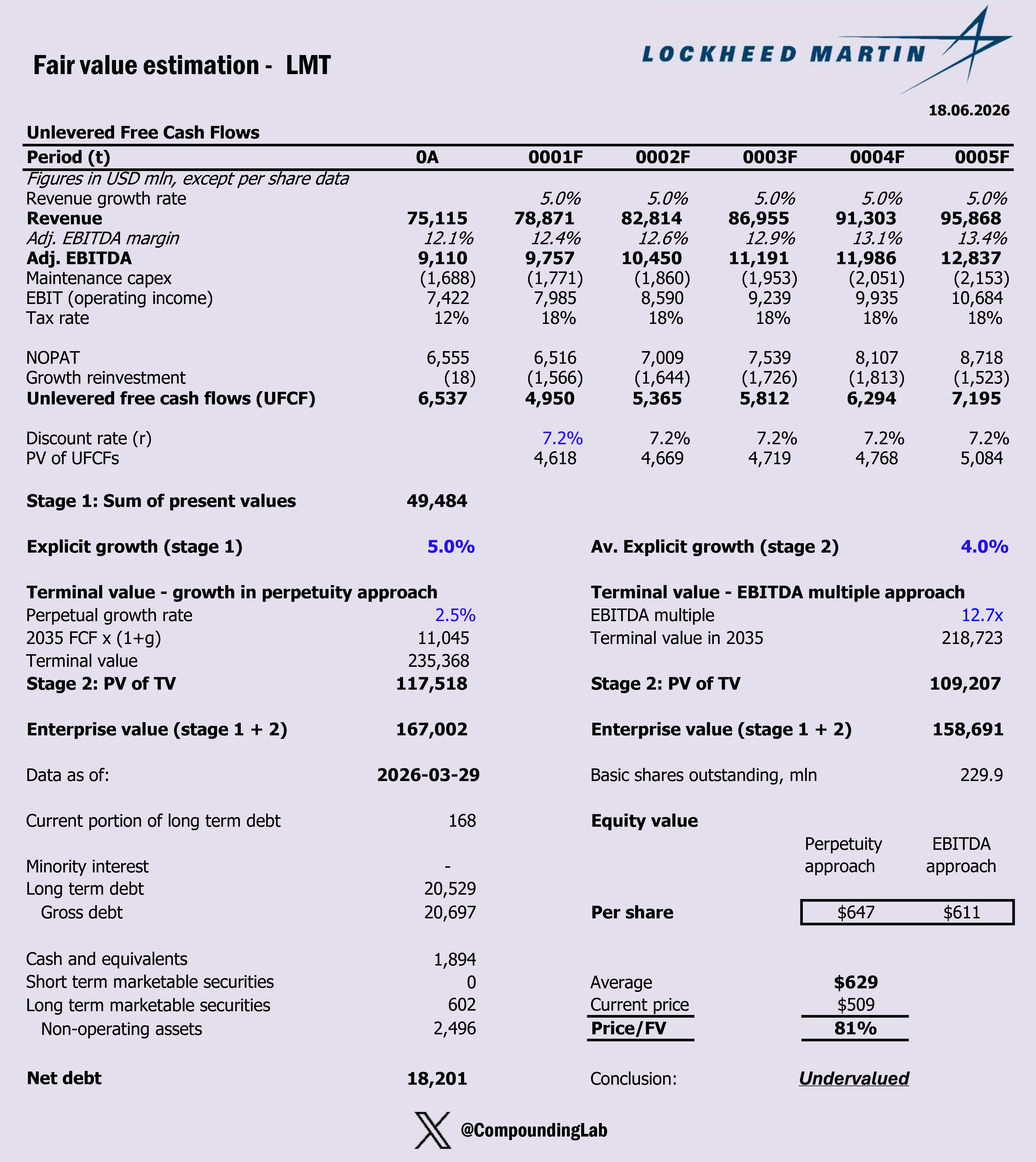

$LMT DCF valuation model

Everyone wants the next exciting growth stock. My Lockheed Martin’s valuation asks a different question: what if a boring defense contractor is being mispriced?

Key assumptions:

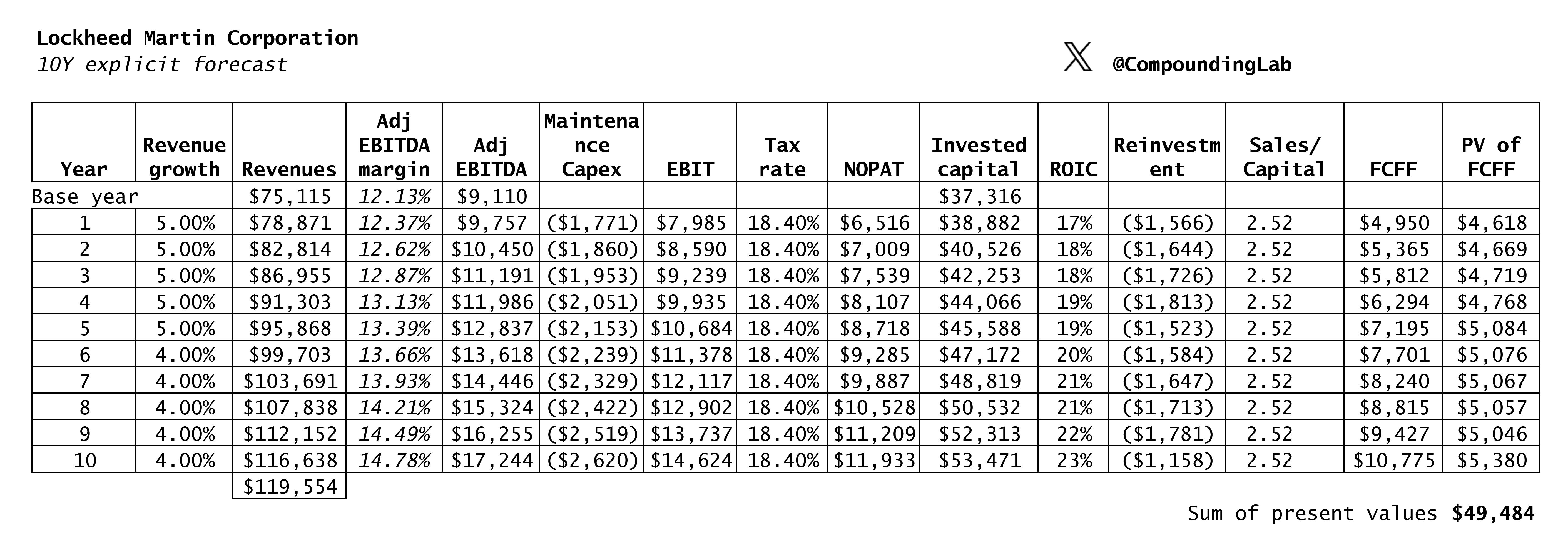

Explicit average 5Y/5Y growth @ 5%/4%

Long-term growth in perpetuity @ 2.5%

EBITDA margin gradual improvement from 12% in Y1 to 14.8% inY10

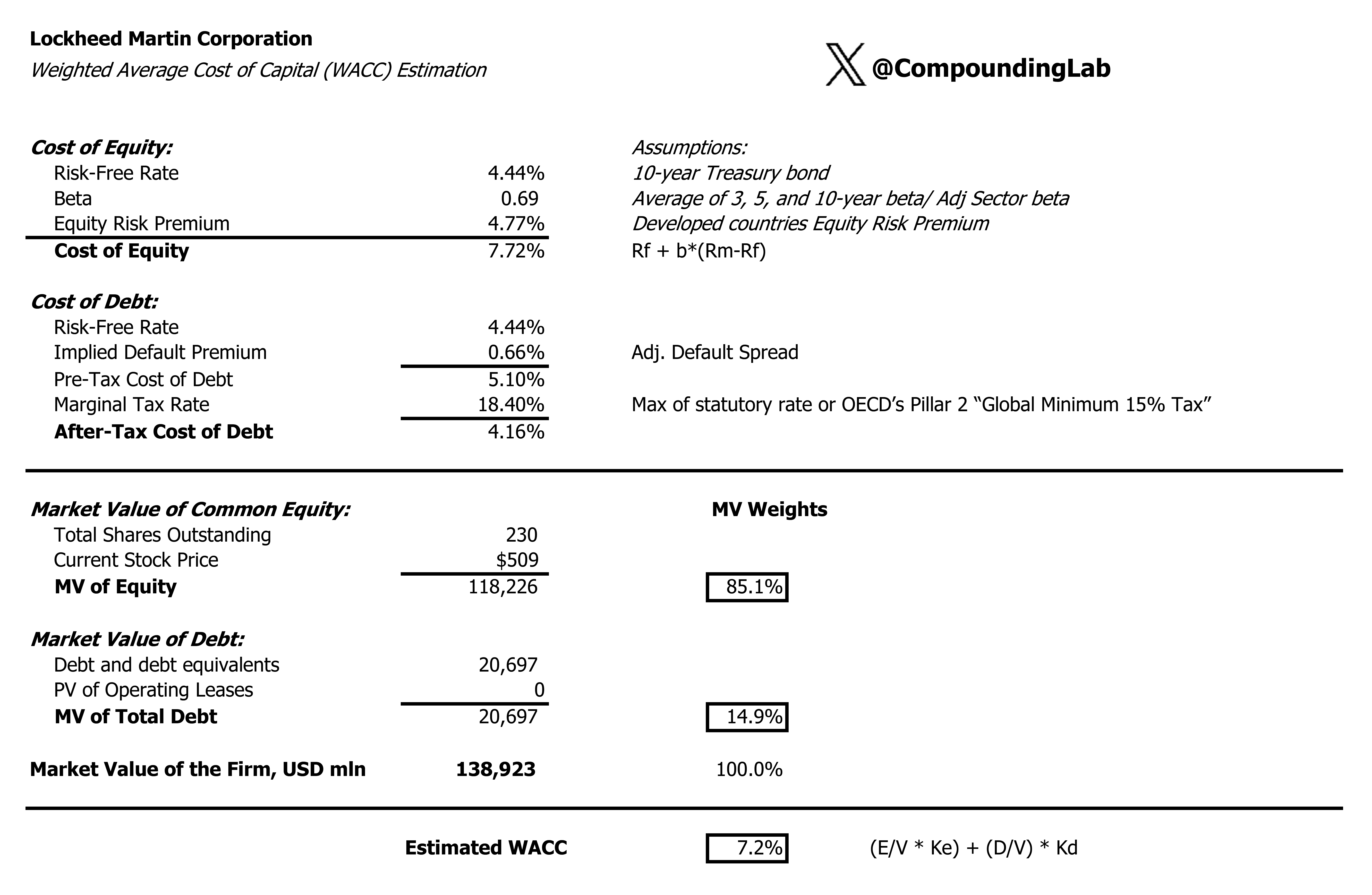

WACC @ 7.2%

Adj. EBITDA exit multiple of 12.7

Tax rate 18%

The input that drives reinvestment is Sales to Capital ratio = 2.5

Historic Growth (for context)

Lockheed was growing at CAGR of 5-6% over the last decade. For my DCF, I am using an initial revenue-growth range of 4–5%, and factoring terminal growth rate of 2.5%. This is consistent with the more relevant post-Sikorsky history. Historical growth rate should not be treated as a recurring benchmark because Sikorsky was acquired in November 2015 and materially lifted the following year’s sales.

Growth rates for defense contractors are naturally correlated with state budgets, which historically have been volatile. My estimated rates are in line with forward-looking estimates for the defense industry in general.

Moat

The defense industry is a rare beast. Despite selling almost exclusively to a single government buyer with shifting requirements and a habit of haggling over costs, the major contractors such as Lockheed Martin, Boeing’s defense unit, BAE Systems, Raytheon, Northrop Grumman, Airbus, and General Dynamics have dominated the rankings for decades without serious outside challengers. The reason is because building weapons is extraordinarily hard. The technology is proprietary, the workforce needs security clearances, and the development timelines stretch across decades rather than years. The F-35 alone took nearly 20 years from contract award to the Marines declaring it combat-ready. Once a contractor wins a program, the government almost never switches suppliers mid-stream; it’s simply faster and cheaper to work out problems with the incumbent than to fund a replacement from scratch. This creates a switching-cost moat. Contract structures reinforce this: early cost-plus deals absorb the government’s development risk, while mature fixed-price production contracts become highly profitable cash flows that can run for 30-40 years when you factor in sustainment. Lockheed’s key franchises sit inside this same logic: mission-critical products, no realistic alternative supplier, and replacement cycles long enough that today’s backlog effectively locks in revenue well into the 2040s and beyond. SpaceX has rattled the launch side of the space business, but the bulk of Lockheed’s space revenue comes from classified strategic programs that Elon Musk has neither the clearances nor the inclination to chase. That is why LMT definitely deserves a wide moat which is fully reflected in my workings. I assume that ROIC will improve gradually from 17% to 23% over explicit forecast period. Terminal value formula (2035 FCF x (1+g)/ (WACC-g)) implies ongoing value creation even behind explicit period, rather than ROIC fading towards cost of capital (in that case one can simply use 2035 FCF x (1+g)/ WACC).

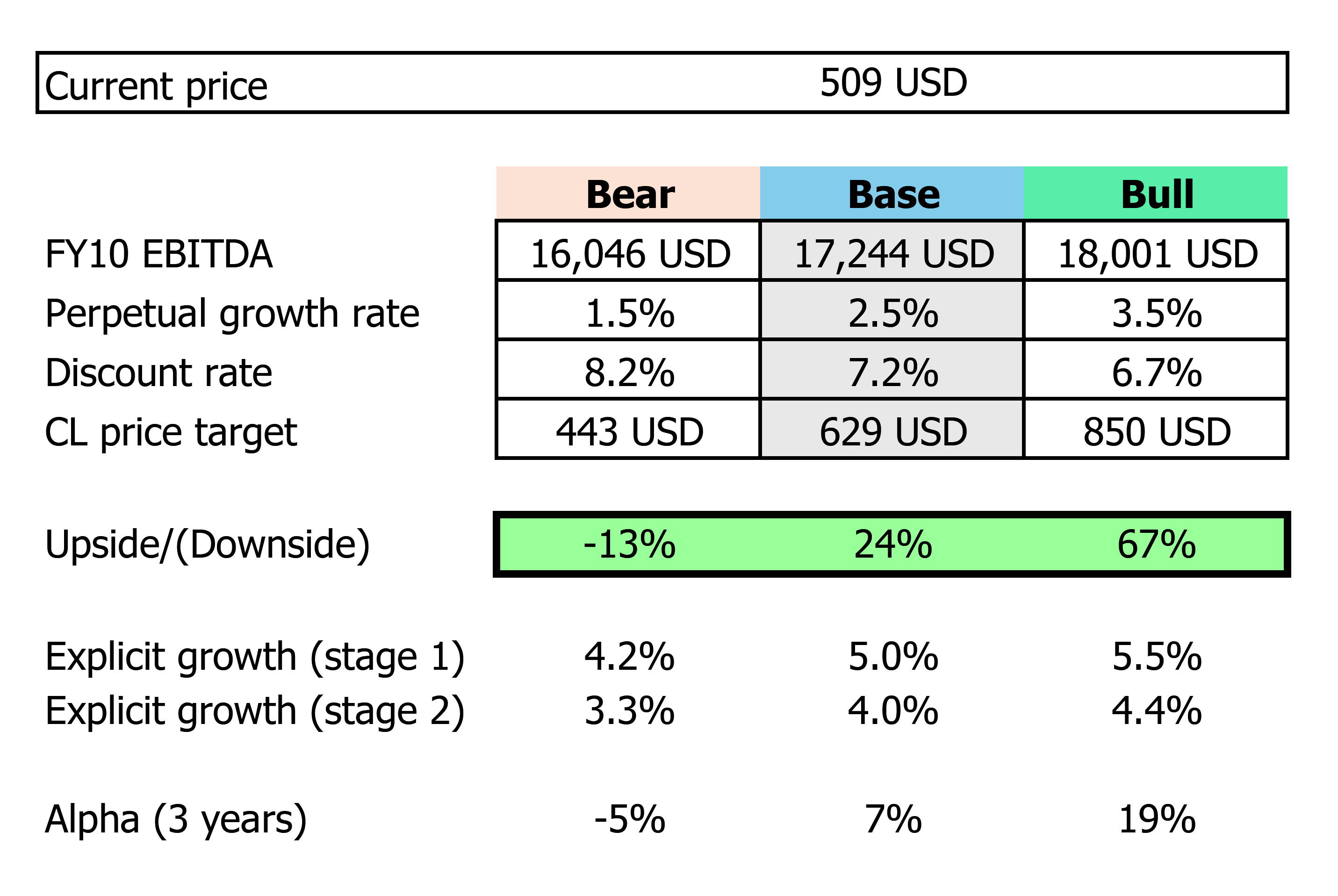

Base case

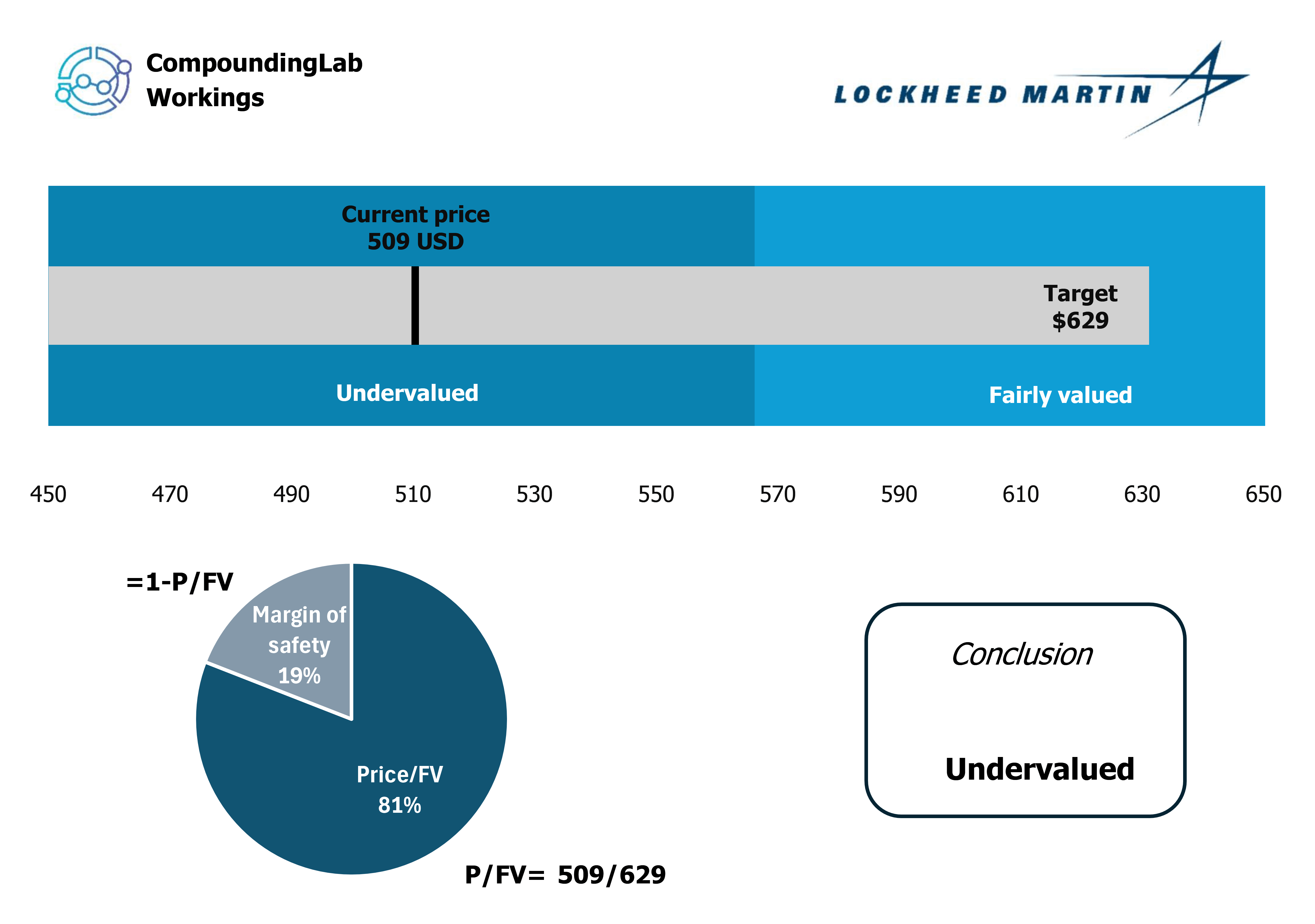

My valuation implies that LMT is trading at roughly a 19% discount to fair value. A move from the current price to $629 over three years would equate to approximately 7% annualized price appreciation. Including the dividend, the potential annual shareholder return could be closer to the high-single digits, assuming the business performs broadly in line with expectations. Here is why my thesis can work well:

Exceptional revenue visibility. Lockheed ended 2025 with a record $194 billion backlog, equal to more than 2.5 years of sales. This gives the company an unusually high degree of revenue certainty relative to most industrial businesses.

Missile-defense demand is accelerating. Patriot PAC-3 and THAAD are becoming increasingly important as the U.S. and its allies rebuild inventories and increase air-defense capacity. Lockheed has agreed to ramp Patriot production from roughly 600 toward 2,000 interceptors annually, while THAAD output is planned to increase from 96 to 400 units per year.

F-35 demand could reaccelerate. The FY2027 U.S. defense budget proposal includes funding for 85 F-35s, compared with 47 in FY2026. A return to higher procurement levels would support Aeronautics revenue, utilization, and eventually margins.

The geopolitical backdrop favors Lockheed’s portfolio. The company is exposed to the exact areas receiving greater defense attention: fighter aircraft, missile defense, precision munitions, naval combat systems, space, and classified programs. The FY2027 budget proposal specifically emphasizes Patriot, THAAD, precision-strike missiles, stockpile replenishment, and F-35 production.

International demand provides an additional growth lever. European, Asian, and Middle Eastern allies are increasing defense spending and seeking proven, interoperable U.S. systems. Lockheed’s installed base matters here: customers buying F-35s, Aegis systems, PAC-3, or Sikorsky platforms also generate long-duration support, sustainment, upgrade, and ammunition demand.

Margins have room to normalize. The market is focused on recent execution problems, production delays, and cost pressure. If Lockheed improves supply-chain throughput and retires program risk, the earnings recovery could be stronger than the market expects. Management maintained its 2026 sales outlook of $77.5–$80.0 billion despite a softer first quarter.

Strong cash-generation potential supports shareholder returns. In 2025, Lockheed generated $6.9 billion of free cash flow and paid meaningful dividends. Even if repurchases remain temporarily limited, the dividend provides a tangible portion of the expected return while investors wait for the valuation gap to close.

What could prevent it from working

Fixed-price contract risk remains the main concern. Cost overruns, supplier shortages, inflation, and execution mistakes can turn revenue growth into lower profitability. Q1 2026 results showed the issue clearly: profit fell as program delays and fixed-price cost pressure weighed on results.

F-16 and C-130 delays could persist. Supply-chain disruptions and production bottlenecks have already affected deliveries. A prolonged issue would hurt both margins and confidence in management’s execution.

Defense spending is political. The FY2027 budget and higher F-35 procurement are proposals, not guarantees. Congress can alter procurement priorities, reduce funding, or shift spending toward drones, software, autonomous systems, and lower-cost platforms.

Government pressure may limit upside economics. Lockheed’s agreement to share excess profits through reinvestment in production capacity may be strategically sensible, but it also shows that the government wants more output and may be less tolerant of exceptional contractor margins.

Buybacks may be less supportive than in the past. The company did not repurchase shares in Q1 2026, partly reflecting pressure to prioritize production capacity. That removes one lever that historically supported per-share earnings growth.

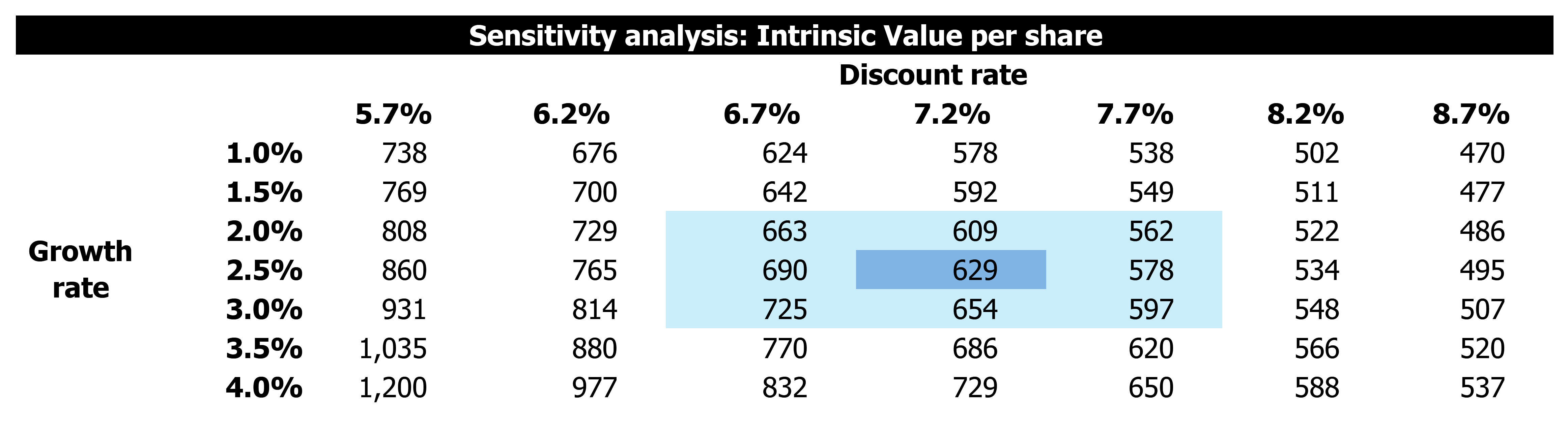

Sensitivity

As always, for prudency purposes I am sharing sensitivity workings, where you can choose your own assumptions as outlined in the tables below.

Feel free to share this article by pressing the button below so that more people can see it.

Verdict

CL model suggests that the stock is currently attractively priced.

___________________________________

Disclaimer: This post is for informational and educational purposes only. I do not own shares in LMT but can buy/sell them at any time after this post is published. Not financial advice. Do your own research.