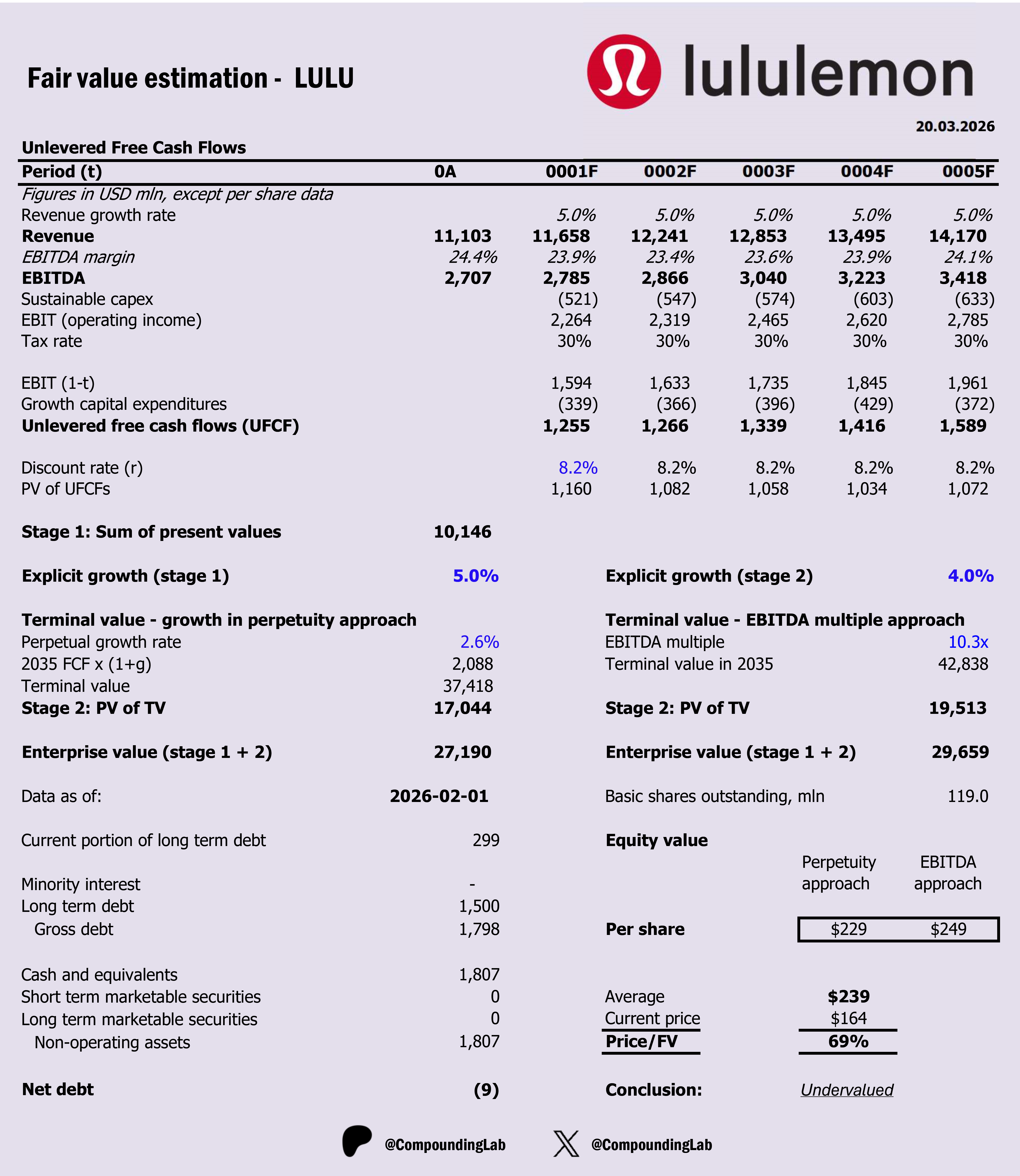

$LULU valuation model (revised)

We have seen elevated volatility in this stock recently and it’s currently in the largest drawdown since 2008. Nevertheless, I’m still holding LULU at a small weight in my portfolio. Today, I am revisiting my DCF workings to understand if it’s still worth holding.

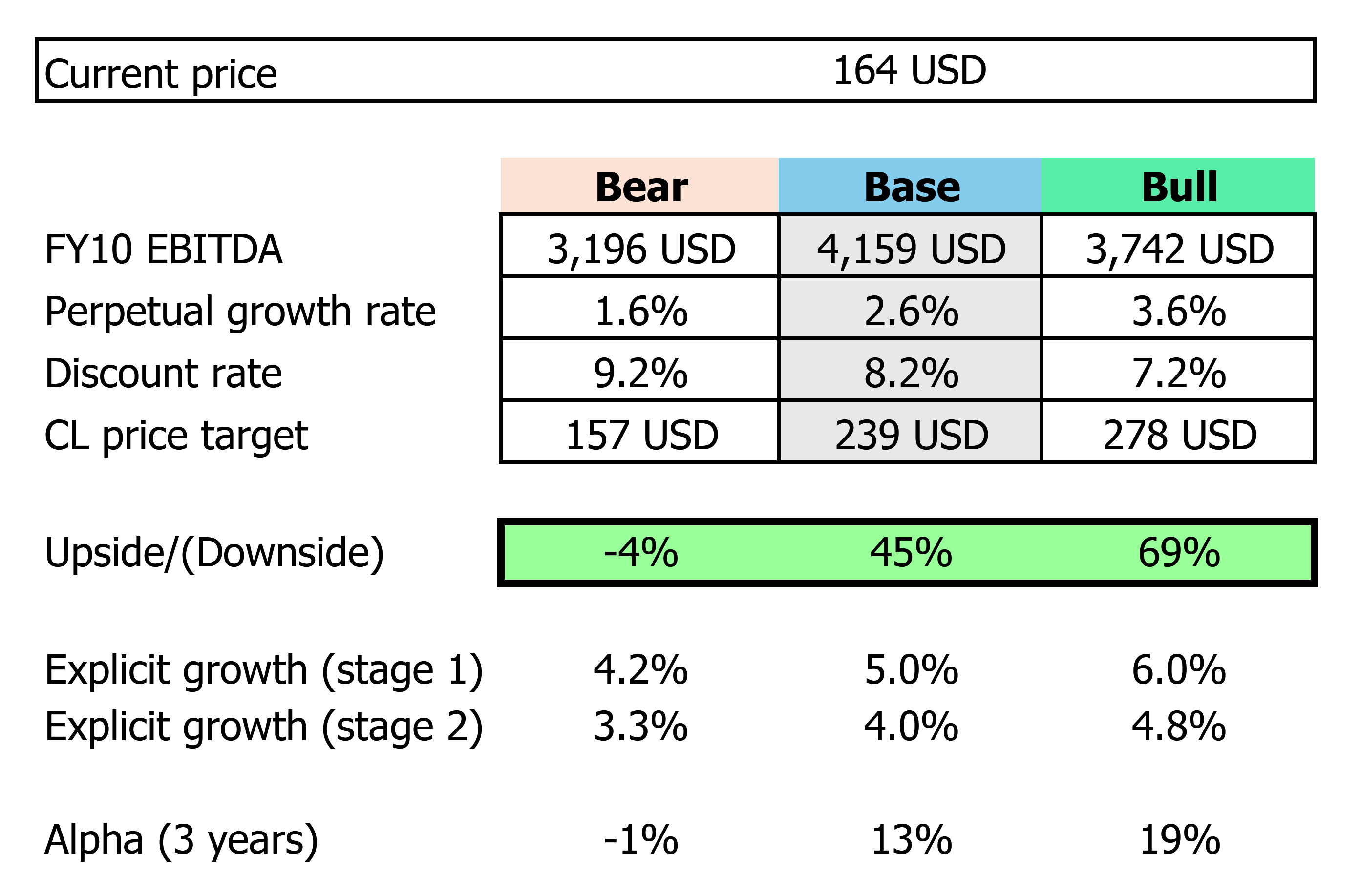

Key assumptions:

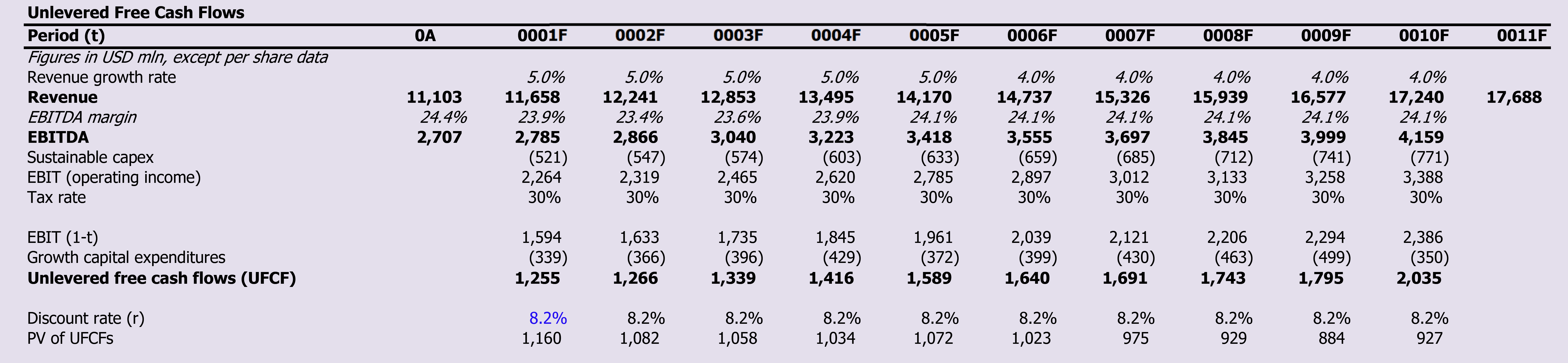

1. Explicit 5Y/5Y growth @ 5%/4%

2. Long-term growth in perpetuity @ 2.6%

3. Near-term margins are under pressure, but over a 5-10 year horizon analysts expect modest improvement, but not a return to peak levels.

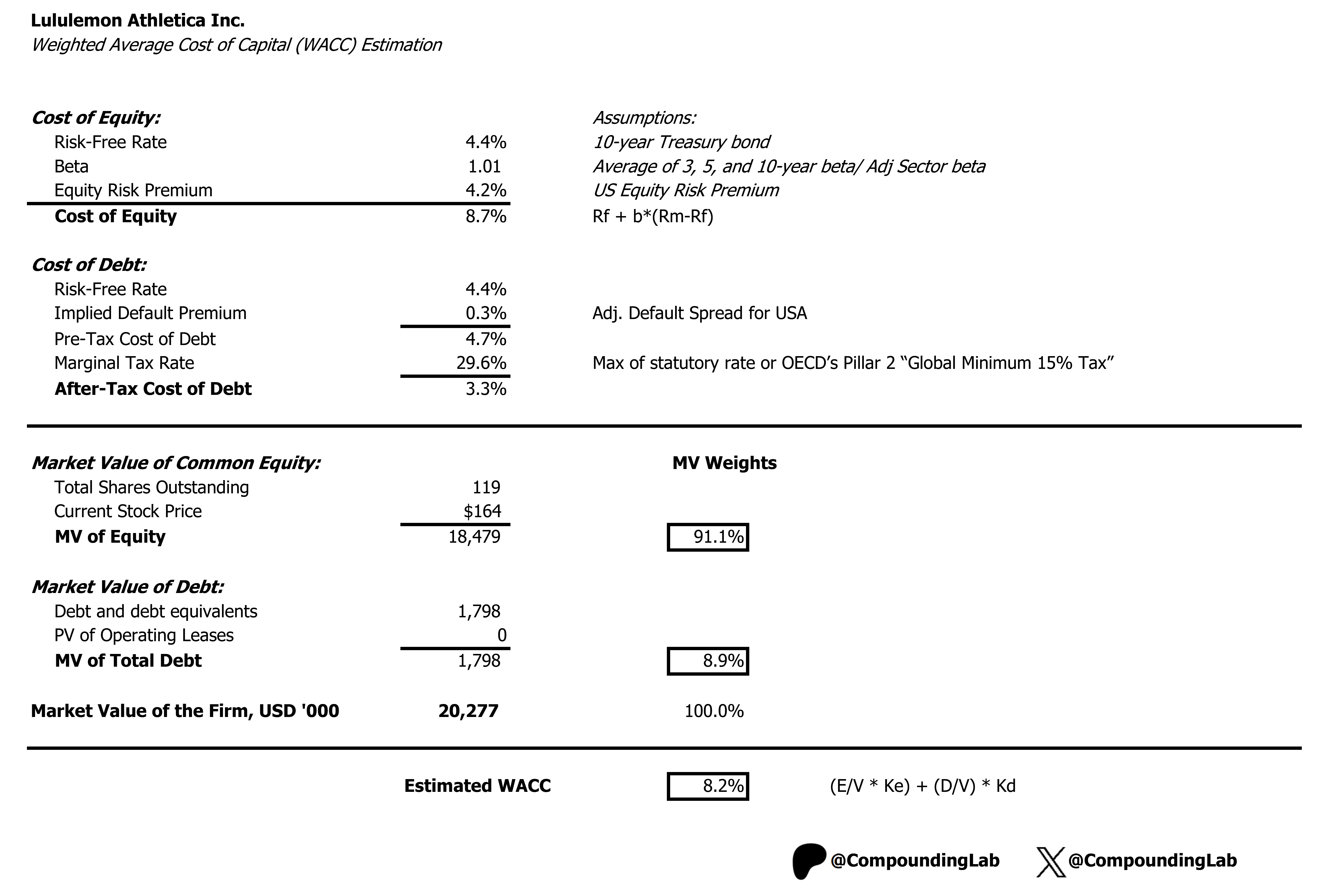

4. WACC @ 8.2%.

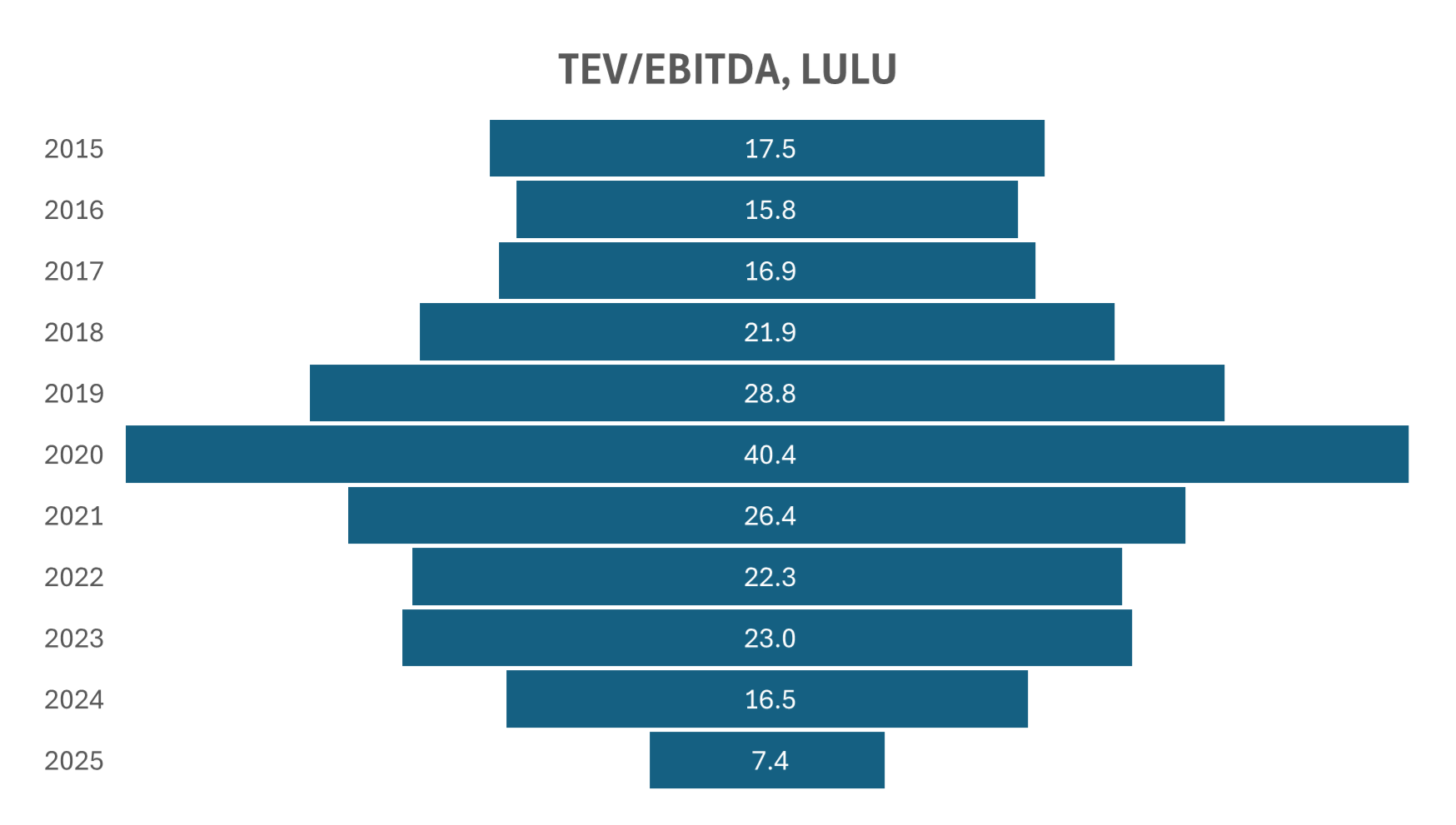

5. An EBITDA exit multiple of 10.3

Although historical values have been much higher, we should not expect a return to those good days in LULU case.

6. Tax rate 30% (historical average)

7. The input that drives reinvestment is the most recent Sales to Capital ratio = 1.7, linearly regressed to the Apparel average rate of 1.28 in year 10.

Historic Growth (for context)

Lululemon Athletica has experienced strong historical growth over the past decade, driven by robust demand in the athleisure market, international expansion, and a focus on direct-to-consumer sales. From 2015 to 2025, the company’s revenue grew at a CAGR of roughly 16-18%, with net income growth slightly higher due to operating leverage. Comparable store sales consistently contributed to topline growth, while gross margins remained strong, supported by premium pricing and a loyal customer base. Expansion into new product categories, like self-care and footwear, and strategic investments in e-commerce have further bolstered long-term growth prospects, positioning Lululemon as a leader in the performance apparel segment.

Expected revenue growth, however, has clearly decelerated vs. its historical phase. In mainland China revenue is expected to grow by approximately 20% in 2026. But, in North America it is projected to decline by 1% to 3% as the company faces persistent demand softness and increased competition in its largest market.

Base case

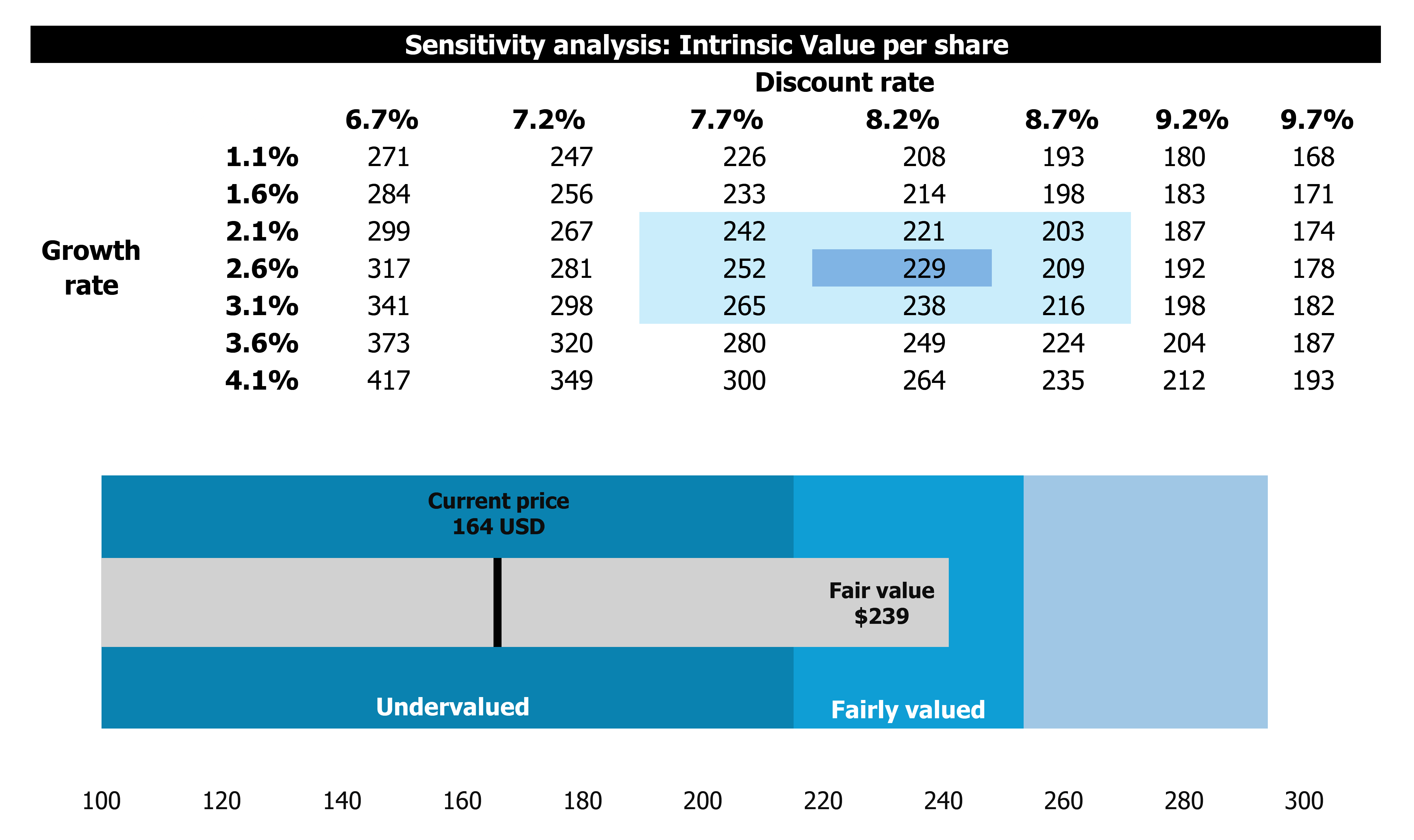

CL intrinsic value for Lululemon is 239$. Valuation suggests that the stock is trading at 31% discount to fair value. If adjusted to FV within 3 years, it will generate annual alpha ~ 13%. Below I highlight why this investment can work well.

Strong brand loyalty and market position. Lululemon has a premium, highly recognizable brand in the athleisure segment. Its products command pricing power, which supports margins and protects from discounting pressures.

Consistent revenue and earnings growth. Historically, Lululemon has delivered high-single-digit to double-digit revenue growth. Expansion into international markets and men’s category provides further growth runway.

Margin expansion potential. Operating margins are high relative to peers, and there is room for further improvement via scaling, supply chain efficiencies, and higher-margin categories like accessories and digital/online sales.

Strong retail and digital presence. A combination of e-commerce and selective retail store expansion allows efficient reach without diluting brand exclusivity. Digital growth also supports better data-driven inventory management and targeted marketing.

Shareholder-friendly policies. Lululemon has a history of share repurchases, which can boost EPS and shareholder returns even without aggressive top-line growth.

Favorable industry tailwinds. Athleisure continues to be a secular trend, with increasing health, wellness, and work-from-home trends sustaining demand. The broader apparel industry had slowly recovered post-pandemic, and this can lift discretionary spending.

Adjustment to intrinsic value. Trading at ~31% discount gives a margin of safety. Mean reversion or multiple expansion could accelerate returns toward fair value.

Experienced management. Lululemon’s leadership has successfully navigated growth, inventory challenges, and international expansion, which increases confidence in execution.

Resilient consumer base. loyal customer base willing to pay premium prices can cushion against economic cycles compared to more commoditized apparel brands.

Sensitivity

If you disagree with me on certain aspects, you can choose your own assumptions based on the table below.

Conclusion

Holding LULU for now, ~3% of portfolio.

Keep in mind that this is an estimate - just like any DCF model. I’m not claiming perfection, but I do trust these calculations to guide my own investments. Hopefully, they can help inform yours as well.

___________________________________

Disclaimer: This post is for informational and educational purposes only. I own shares in LULU and can buy/sell them at any time after this post is published. Not financial advice. Do your own research.