$MELI DCF valuation model - updated

Key assumptions:

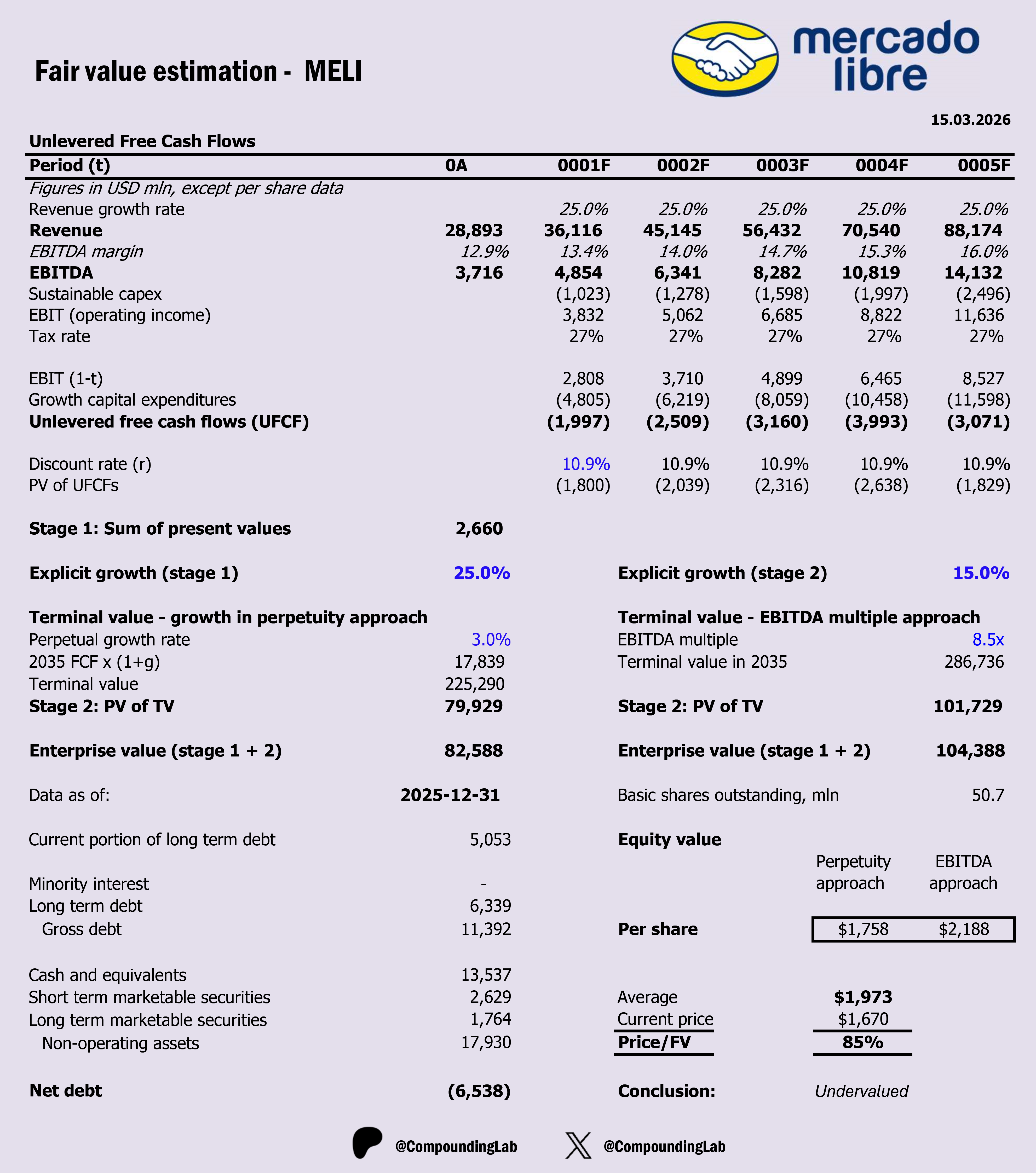

1. Explicit 5Y/5Y growth @ 25%/15%

2. Long-term growth in perpetuity @ 3%

3. Adjusted EBOTDA margin expansion from 13% to 20% in 2035.

4. WACC @ 10.9%

5. An EBITDA exit multiple of 8.5

6. Tax rate 27%

7. The input that drives reinvestment is the linearly regressed Sales to Capital ratio, from 1.9 recently to 1.3 in 2035

Historic Growth (for context)

MercadoLibre has delivered exceptional historical growth, evolving from a regional marketplace into Latin America’s dominant e-commerce and fintech ecosystem. Over the past decade, revenue has compounded at well over 25% annually, driven by rapid expansion in Brazil, Mexico, and Argentina, surging logistics capabilities, and the explosive adoption of MercadoPago. Gross merchandise volume, unique buyers, and fintech TPV have all scaled dramatically, while EBITDA has expanded from modest levels to billions as the company gained operating leverage. This combination of platform effects, fintech penetration, and sustained demand for digital commerce has made MELI one of the fastest-growing large-cap companies globally - setting the backdrop for any forward-looking valuation.

Why I believe it can work out well

Sustained high revenue growth

Fintech flywheel gaining momentum

Logistics moat is strengthening

Operating leverage over time

Large TAM still underpenetrated

Ecosystem effects reinforce growth

Strong balance sheet and disciplined execution

Optionality from new verticals

What can go wrong

Margin pressure persists

Credit risk in fintech

Currency volatility

Intensifying competition

Regulatory risk

Macro instability

Execution missteps

Conclusion

My intrinsic value for MercadoLibre is 1,973$. Valuation suggests that the stock is trading at 15% discount to fair value. If adjusted to FV within 3 years, it will generate +6% in annual alpha.

___________________________________

Disclaimer: This post is for informational and educational purposes only. I don’t own shares in MELI but can buy/sell them at any time after this post is published. Not financial advice. Do your own research.