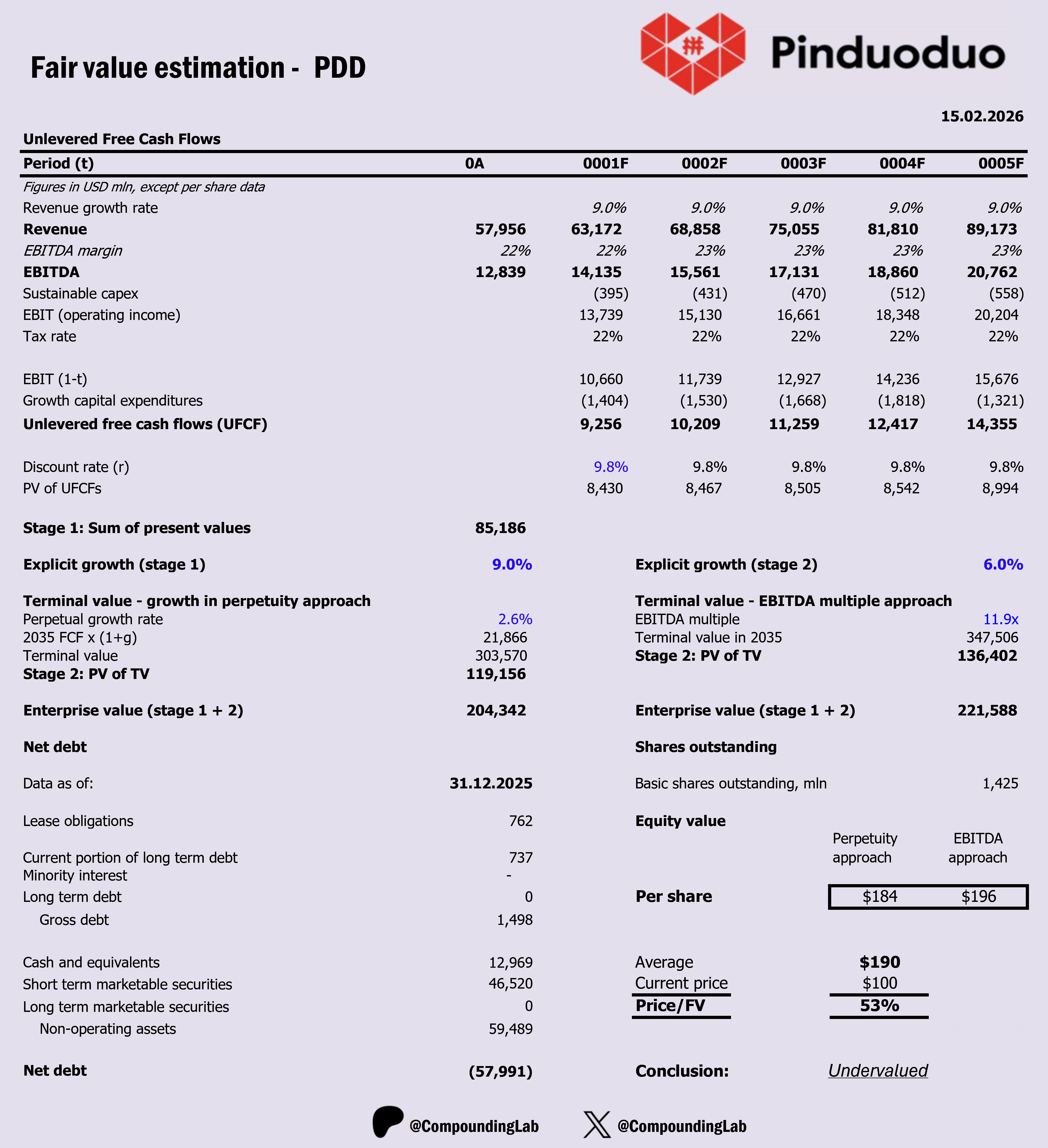

$PDD DCF valuation model

Key assumptions:

1. Explicit 10Y growth @ 6-9%

2. Long-term growth in perpetuity @ 2.6%

3. 22% EBITDA Margin, gradually improving as sales and marketing costs go down as a % of revenue.

4. WACC @ 9.8%.

5. An EBITDA exit multiple of 11.9

6. Tax rate 22%

7. The input that drives reinvestment is Sales to Capital ratio = 4

Conclusion: Valuation suggests that the stock is trading at 47% discount to fair value. If adjusted to FV within 3 years, it will generate 24% in annual alpha. Therefore, I will make a small entry tomorrow (<2% of the portfolio).

Very close to:

https://open.substack.com/pub/absolutetoal/p/discounted-eps-gap_rsp-value-formula?utm_source=share&utm_medium=android&r=5g11d4

9.8% Wacc is too high due to the speculative BETA.

Wacc is not the real economy cost of capital, just a speculative figure.

Clean Invested Capital Cost (CICC)

=

100

×

{

[1 + 30Y Treasury Notes Yield Ratio]

×

[1 + D/E × (1 + Prime_Ratio + Spread Ratio)]

÷

[1 + D/E]

- 1

}

= 100×(1.04696×(1+0.027270204×(1+0.07+0.03))÷(1+0.027270204)-1)

= 4.9739289487%

.

EPV (NON-GAAP, Fin.2025.09.Q3.TTM)

= Non-Gaap EPS ÷ CICC

= 11.1539496765÷0.0497392895

= USD 224.2482711077