$TROW

$TROW is trading like a broken asset manager - but the math says it’s being priced like a melting ice cube while still earning elite returns and carrying zero debt. Either the business is quietly deteriorating… or the market is badly misreading it. I ran the numbers - they don’t match the narrative.

Introduction

T. Rowe Price looks like a value trap at first glance.

Years of stock underperformance versus the S&P 500 and persistent outflows from active funds have pushed sentiment into the basement.

But underneath the weak chart sits a business with double-digit returns on capital, fortress balance sheet, and margins most asset managers would envy.

This disconnect between price action and business quality is exactly where mispricings tend to form.

So let’s walk through the fundamentals visually and see what the market may be missing.

Scoreboard

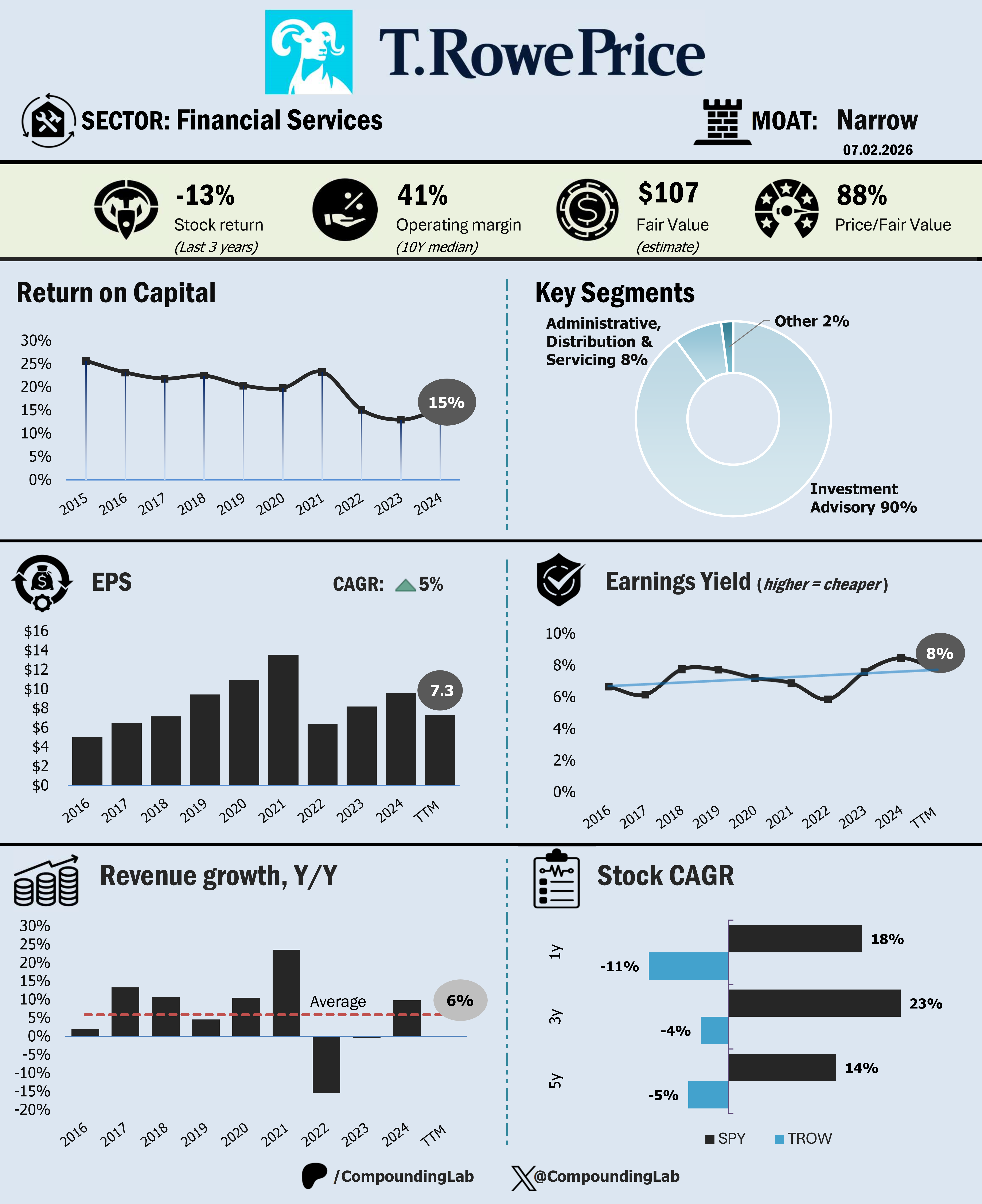

Over the last 1 year, the S&P 500 is up about +18% while $TROW is down roughly -11%.

Zoom out to 3 years: SPX +23%, TROW -4%.

Five years: SPX +14%, TROW -5%.

That’s not underperformance. That’s sustained neglect.

The most recent 1-year lag is mostly sentiment-driven. Active managers have been out of favor, passive keeps taking share, and fee pressure headlines never stop. Add market mix effects and net outflows, and the stock gets treated like a structurally shrinking franchise - even though the core economics remain strong.

Return on invested capital tells a different story. 10-year median ROIC sits around ~19%. That’s not average. That’s elite for a scaled financial franchise. Businesses that consistently compound near 20% on capital are rarely “broken” - they’re usually mispriced when sentiment turns.

How about Balance sheet? It looks practically armored. Debt/Equity ~ 0%. No leverage story. No refinancing risk. No hidden time bomb. In a cyclical, market-sensitive industry, that matters more than most investors give credit for.

Now let’s look at valuation through earnings power.

Current earnings yield ~8% - which decomposes into solid operating margin, high capital efficiency, and modest reinvestment needs. You’re not paying growth-stock multiples for this stream. You’re paying late-cycle skepticism multiples.

Moat rating is Narrow, and that’s fair. The edge comes from brand, distribution, retirement channel strength, and long performance records across strategies. Not unbreakable - but sticky enough to support excess returns over time.

Growth hasn’t been flashy, but it’s been durable. Historical revenue growth around ~6%. Forward expectations closer to ~4% (although dependent on market performance), roughly in line or slightly below industry asset growth assumptions. This is not a hyper-growth manager. It’s a steady compounder with operating leverage.

Market share remains meaningful in active mutual funds and retirement channels, where T. Rowe Price still ranks among the largest U.S. players. The business mix is diversified across equity, multi-asset, and retirement solutions - not a one-product shop.

Revenue is primarily consists of investment advisory fees, with smaller contributions from administrative and distribution services. Yes, account counts are drifting lower - but asset management is a fee-on-assets business, not a headcount business. The real battle is product mix and flows, not customer tallies.

Operating margin runs near 41%. For asset management, that’s strong. It signals pricing power, scale efficiency, and disciplined cost control - not distress.

Drawdowns historically have been sharp but cyclical - often tied to bear markets and fee compression scares - and repeatedly followed by multi-year recoveries when flows and markets stabilize.

Now let’s plug numbers into the Mauboussin framework. With ROIC ~18% and forward growth around ~4%, justified P/E lands near ~15x. The stock trades closer to ~10x. That gap is my valuation signal.

Intrinsic value estimate comes out near $107 per share. At a current price around $95, that’s roughly a 12% discount.

Conclusion

TROW does not resemble a hype story.

Rather, a quality business priced like a declining one - and that tension is where the opportunity lives.