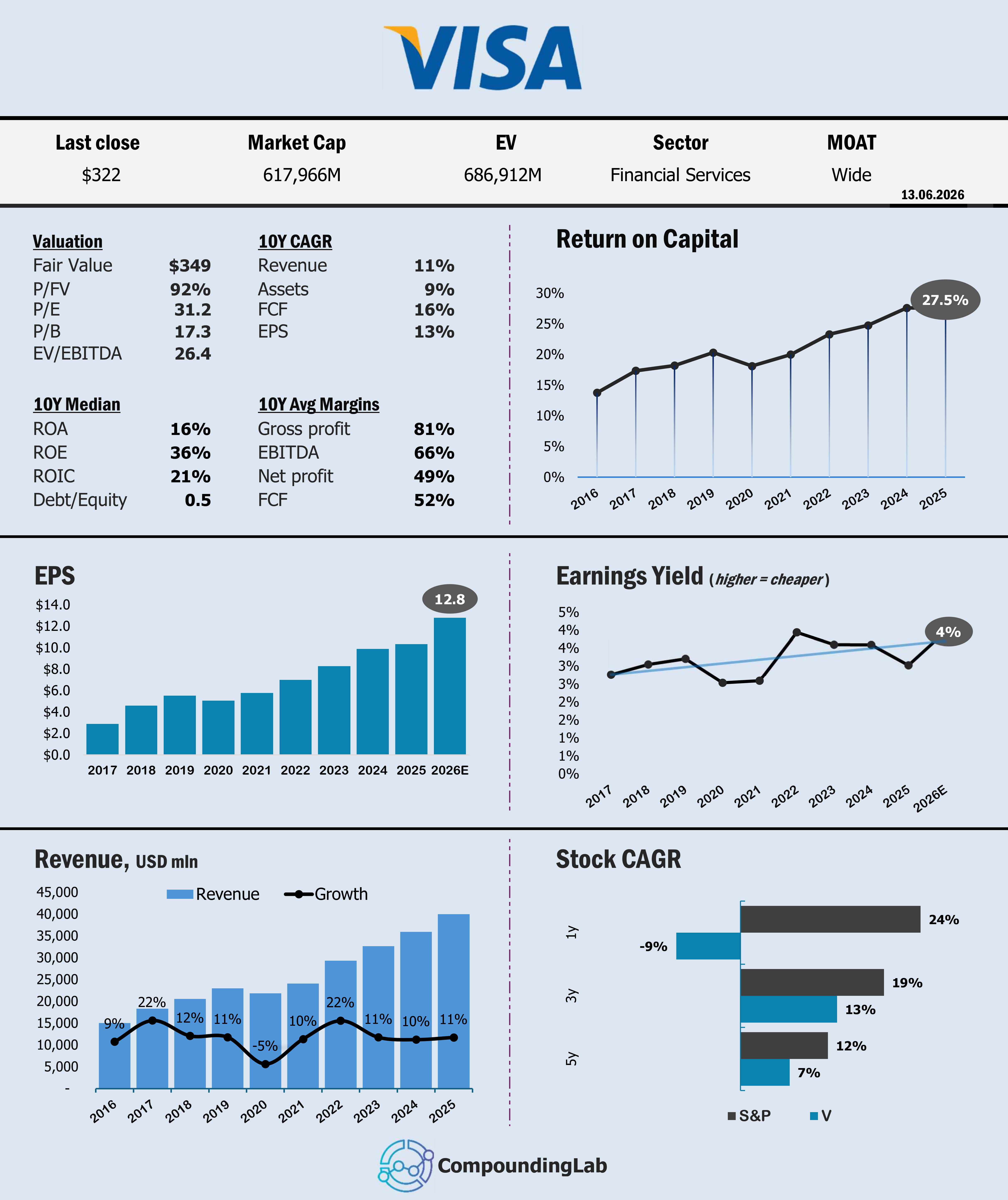

VISA – valuation model

Why I see upside in the World's Payment Toll Road

The Thesis

If you’ve ever tapped your card at a coffee shop, bought something online in another country, or paid for a streaming subscription, there’s a very good chance Visa took a small slice of that transaction - quietly, invisibly, and almost certainly without you thinking about it. That’s the business I’m writing about today.

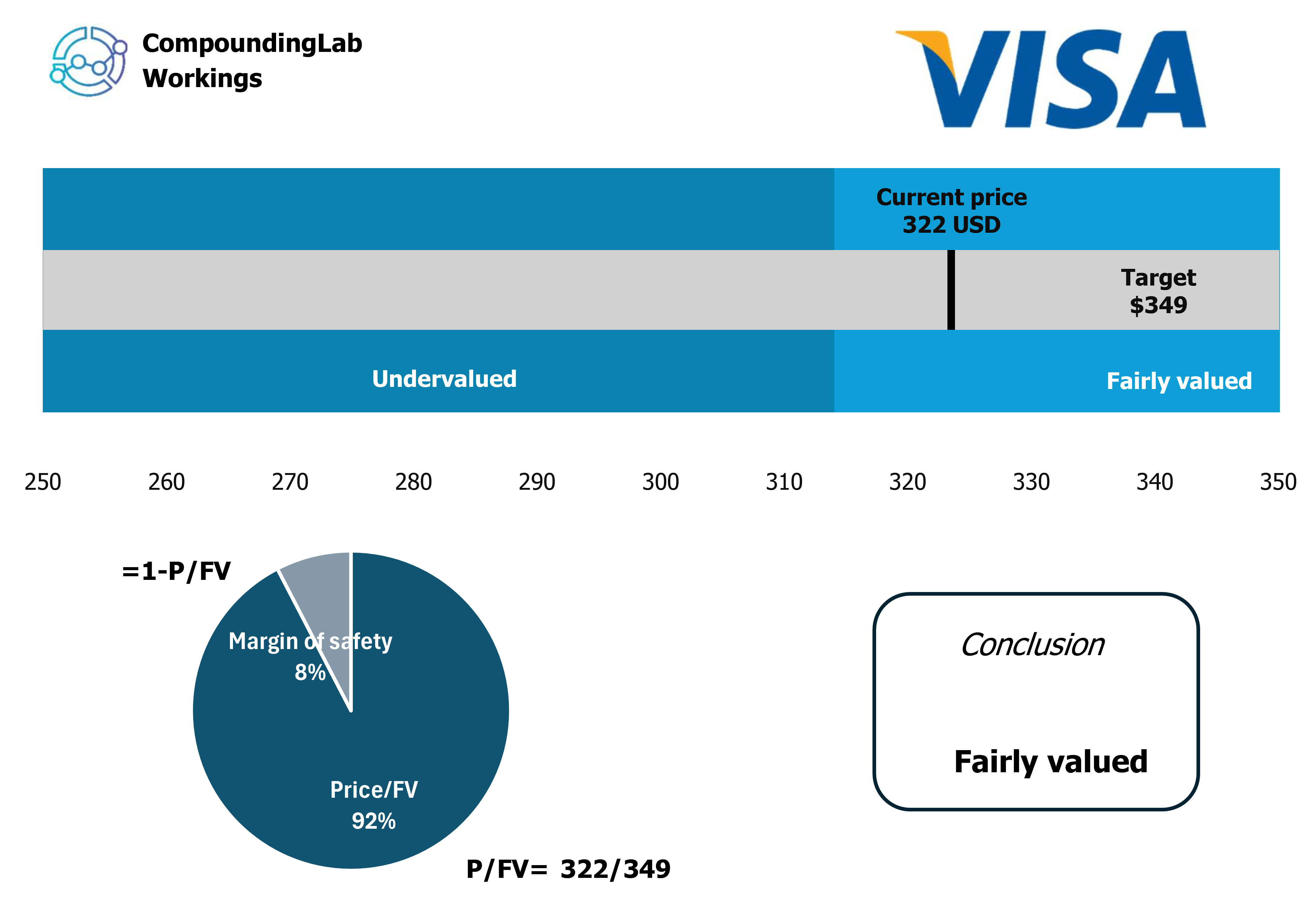

I’m initiating coverage of $V with a BUY rating and a price target of $349, representing roughly 8% upside from current levels. My conviction rests on three pillars: an irreplaceable global network that keeps getting bigger, a high-growth Value-Added Services segment that’s expanding the monetization opportunity well beyond payment processing, and the simple arithmetic of a capital-light model that turns revenue growth into free cash flow at an exceptional rate.

Visa is not just a payments company. It is increasingly a network of networks - an infrastructure layer connecting consumers, banks, merchants, blockchains, and real-time payment systems across more than 200 countries. That positioning is worth paying attention to.

The stock has pulled back from its 52-week high of $375 and currently trades at $323. I think that creates a reasonable entry point for a business with a demonstrated ability to compound earnings in the high-teens over time. Let me walk you through my thinking.

What Visa Actually Does

Visa does not lend money. This is the most important thing to understand about the business model. Visa is not a bank. It does not take credit risk. It does not hold loans on its balance sheet. What it does is run the plumbing - the global network that authorizes, clears, and settles electronic payment transactions between cardholders, merchants, and the financial institutions that issue cards and acquire merchant accounts.

In fiscal 2025, Visa’s scale remained extraordinary: 329 billion Visa-branded payment and cash transactions were facilitated by Visa or partner networks, while Visa’s own networks processed 257.5 billion transactions. The ecosystem included 4.9 billion payment credentials, nearly 14,500 financial institutions, and more than 175 million merchant locations globally. Scale is everything here - it creates the self-reinforcing dynamic where more issuers attract more merchants, which attracts more issuers, making the network progressively harder to displace.

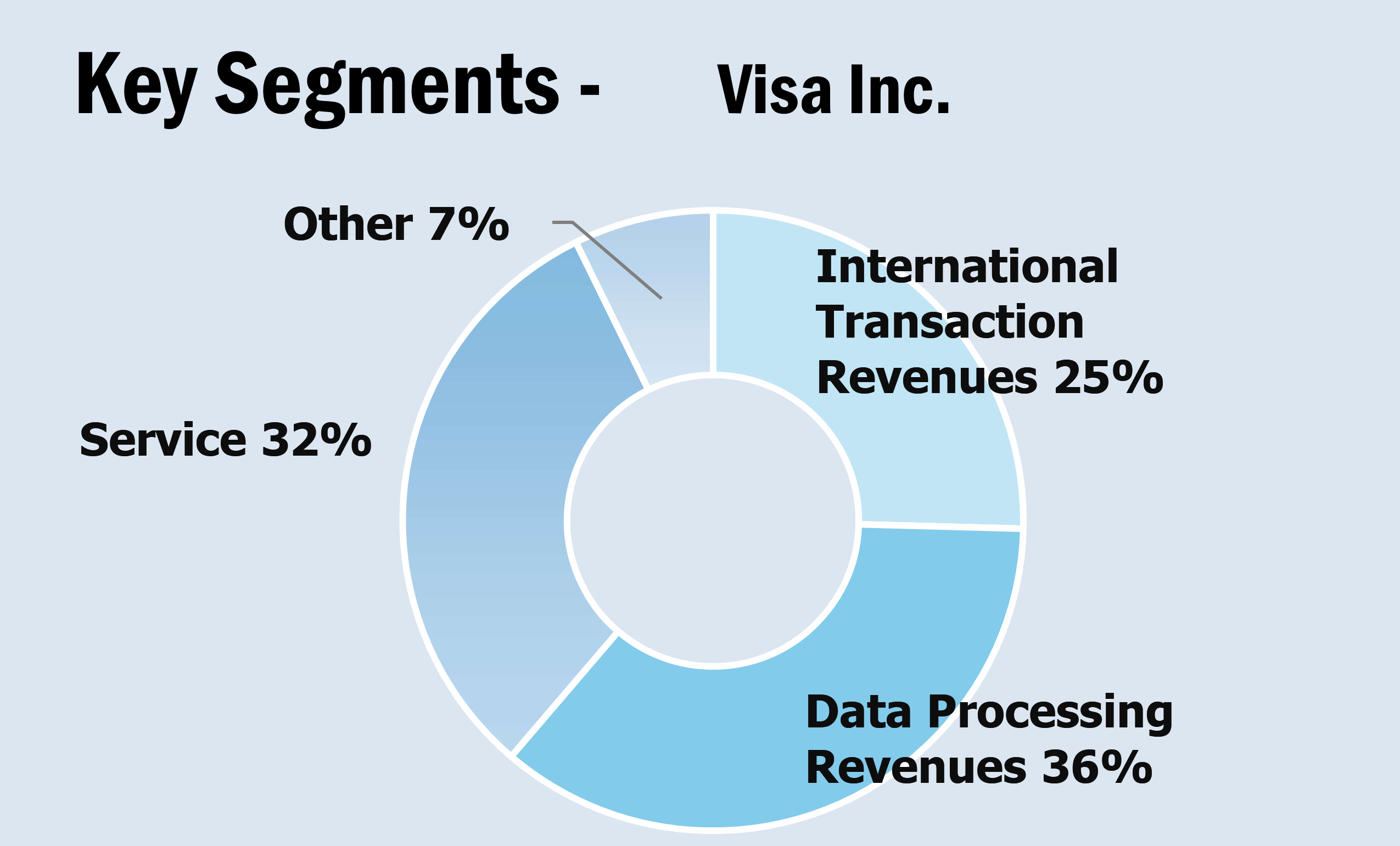

Revenue is organized into four segments. Service Revenue (32% of total) is earned as a percentage of total payment volume. Data Processing Revenue (36%) is earned per transaction, regardless of dollar amount. International Transaction Revenue (25%) comes from cross-border activity and currency conversion. The remaining 7% is Other Revenue - primarily Value-Added Services like fraud prevention and tokenization - and it is by far the fastest-growing part of the business.

2025 Revenue by Segment

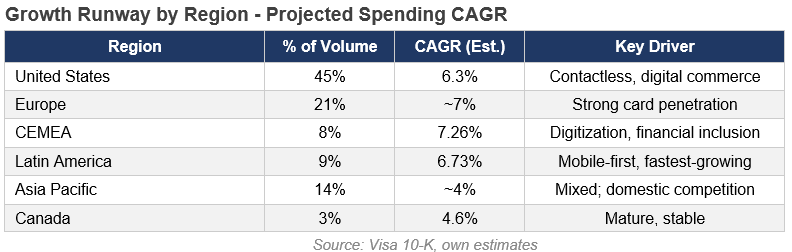

Geographically, the United States drives 45% of total spending volume. Europe accounts for 21%, Asia Pacific 14%, Latin America 9%, CEMEA 8%, and Canada 3%. The growth story is increasingly international, with the highest-growth regions being ones where digital payment infrastructure is still being built.

What Drives the Investment Case

1. The Global Shift to Digital and Contactless Payments

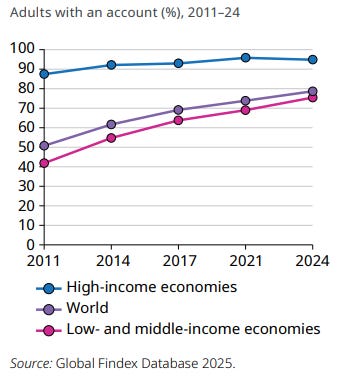

The multi-decade structural shift away from cash toward electronic payments is probably the single most powerful tailwind in Visa’s story. Global bank account ownership rose from 51% to 79% between 2011 and 2024 - a 3.42% annual growth rate - with much of that increase coming from emerging markets where governments are actively pushing financial inclusion and mobile-first banking.

In Latin America specifically, Visa’s total volume grew at a 12.2% five-year CAGR. As governments continue digitizing their economies, Visa benefits as the infrastructure through which digital transactions flow. I model total transaction volume growing at a 6.2% annual rate over my 10-year forecast horizon.

2. An Unassailable Network and Pricing Power

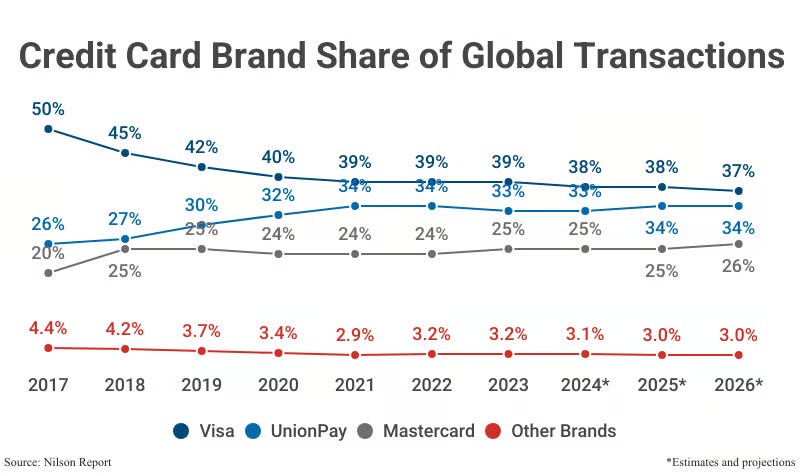

Visa processes 38% of international transactions and 61% of U.S. domestic transactions. Together with Mastercard, these two networks account for 90% of processing activity outside China. That’s a duopoly built over decades that shows no signs of structural erosion.

The network effect here is as powerful as it gets. Every new merchant that accepts Visa makes the card more valuable to cardholders. Every new cardholder makes acceptance more attractive to merchants. This flywheel has been spinning for decades, and the result is a moat that would cost tens of billions of dollars and many years to replicate.

Visa has raised its take rate every single year for the past decade while growing volume simultaneously. In an industry where every basis point matters, that combination is an extraordinary demonstration of pricing power.

Service Revenue per dollar of spending has increased from 0.097% in 2020 to 0.125% in 2025. Data Processing Revenue as a share of transaction volume has risen from 5.4% to 6.1%. I expect both trends to continue at 2.0% and 1.5% CAGRs respectively through my forecast period.

3. Value-Added Services: The Engine Within the Growth Story

The most exciting part of Visa’s story today is not core payment processing - it’s what’s growing alongside it. The Value-Added Services segment has expanded at a 23% CAGR over the past three years against 11% growth for total revenue. It is now Visa’s fastest-growing business and, I believe, the segment most investors are underestimating.

VAS includes fraud prevention and tokenization tools, risk scoring, identity verification, acceptance solutions for small merchants, issuing solutions for fintechs and banks, advisory services, and licensing fees. Many of these services can be delivered independently of Visa’s core payment network - meaning Visa can earn revenue from parties that route transactions over other rails.

Visa is inserting itself into blockchain ecosystems and real-time payment networks as the trust and interoperability layer, becoming a first mover in networks like Tempo and Canton. This turns former competitive threats into revenue opportunities. I project VAS to grow at an 18.3% CAGR from $4.1B today to $21.8B by 2035, representing 15.4% of total revenue.

The Financial Engine

Revenue: Four Streams, One Direction

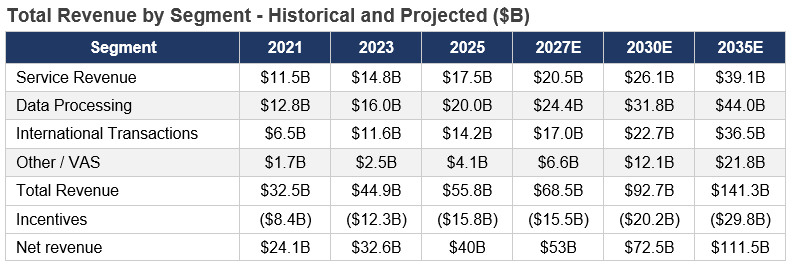

Net revenue has compounded at roughly 11% annually over the past decade and I expect that pace to continue, reaching $103B by 2035 from $43B today - an 8.9% CAGR. Each operating segment contributes a distinct and mutually reinforcing growth story.

Data Processing Revenue ($20B) grows with transaction counts. As tap payments, subscription billings, and digital commerce add transaction frequency, this line grows mechanically - I project an 8.2% CAGR to $44B by 2035. Service Revenue ($17.5B) is tied to spending volume; I project an 8.3% CAGR to $39B. International Transaction Revenue ($14.2B) benefits from the boom in cross-border e-commerce, growing at 8.7% annually through 2030 - I project a 9.9% CAGR to $36.5B.

Total Revenue by Segment - Historical and Projected

Margins: Exceptional and Durable

Visa’s operating economics are among the best of any large-cap company I follow. The five-year average operating margin is 64% and net margin has averaged 52%. These reflect the genuine economics of a platform business that incurs negligible marginal costs to process each additional transaction.

Client Incentives - rebates paid to financial institutions to win card issuance and routing - have grown as a percentage of revenue from 18.4% in 2016 to 28.3% in 2025, as Visa fights harder for relationships in emerging markets. This is margin pressure, but it is the right kind: Visa is investing in long-term network lock-in. I expect operating margins to remain in the 41-45% range through my forecast period.

What I find remarkable is the margin resilience during downturns. During COVID-19 in 2020, Visa’s revenue declined 2.2% - but net margin only compressed to 38.1%. Because costs scale with transaction volumes, cost and revenue move together, providing a natural hedge against economic shocks.

Capital Allocation: Disciplined and Shareholder-Friendly

Visa’s capital requirements are genuinely low. The core network is already built and globally scaled - incremental transactions flow through at essentially zero marginal infrastructure cost. Ongoing CapEx (averaging 2.5% of revenue) is focused on cybersecurity, software for VAS, and data center maintenance, not capacity expansion.

This leaves enormous free cash flow. I project FCF growing from $21B in FY2026 to $50B by FY2035. Management deploys this overwhelmingly through buybacks - historically around 82% of net income. Going forward I model buybacks at approximately 70% of net income as the dividend grows modestly. Leverage is conservative at 0.69x Debt/Equity, declining to 0.50x by 2035, with Interest Coverage at a comfortable 42x.

Competitive Positioning

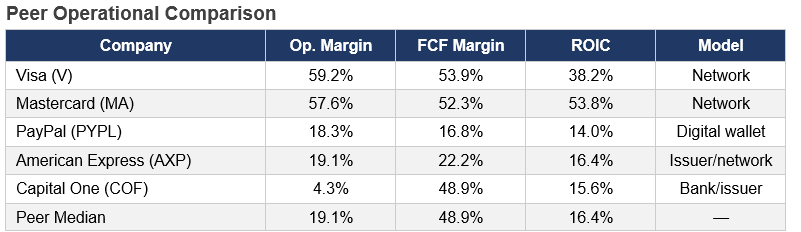

The payments industry is, at its core, a scale game. Visa and Mastercard have decades of accumulated scale, issuer relationships, and merchant acceptance infrastructure that newer entrants cannot replicate quickly or cheaply. Together, these two networks account for 90% of processing activity outside China.

Visa and Mastercard operate in a different economic universe from every other peer. Operating margins near 60%, FCF margins above 50%, ROIC multiples of what banks and fintechs generate - these numbers reflect a structural advantage that derives from the network model itself. They don’t take credit risk. They scale with volume.

The Visa vs. Mastercard dynamic: both grow as digital payments displace cash, and neither is aggressively trying to take share from the other. Visa leads on card count (4.8B vs. 3.15B) and U.S. domestic share. The rivalry is stable and mutually beneficial.

The more interesting competitive question is about alternative rails. Account-to-account (A2A) payment systems, real-time networks like Brazil’s Pix and India’s UPI, and stablecoins all represent potential share-takers. Visa’s response - becoming the interoperability layer between fragmented systems rather than competing with them head-on - is exactly the right strategic posture. By bridging incompatible networks, Visa charges routing and conversion fees in the same way it charges on cross-border transactions today.

Return on Invested Capital: The Quality Signal

I spend a lot of time on ROIC because it is the single metric that best reflects whether a business is genuinely compounding value or just growing. Visa’s ROIC has risen from 13.8% in 2016 to 27.5% in 2025, and I expect it to reach approximately 63% by 2035 as invested capital turnover improves with volume growth.

What drives the ROIC improvement is the capital-light nature of the model. Invested capital is dominated by Goodwill ($19.9B) and Other Intangible Assets ($27.6B) from past acquisitions - items that don’t need to grow proportionally with revenue. As revenue and NOPAT scale faster than the capital base, Invested Capital Turnover improves from 58% in 2025 to 136% by 2035. That improvement is essentially baked into the business model.

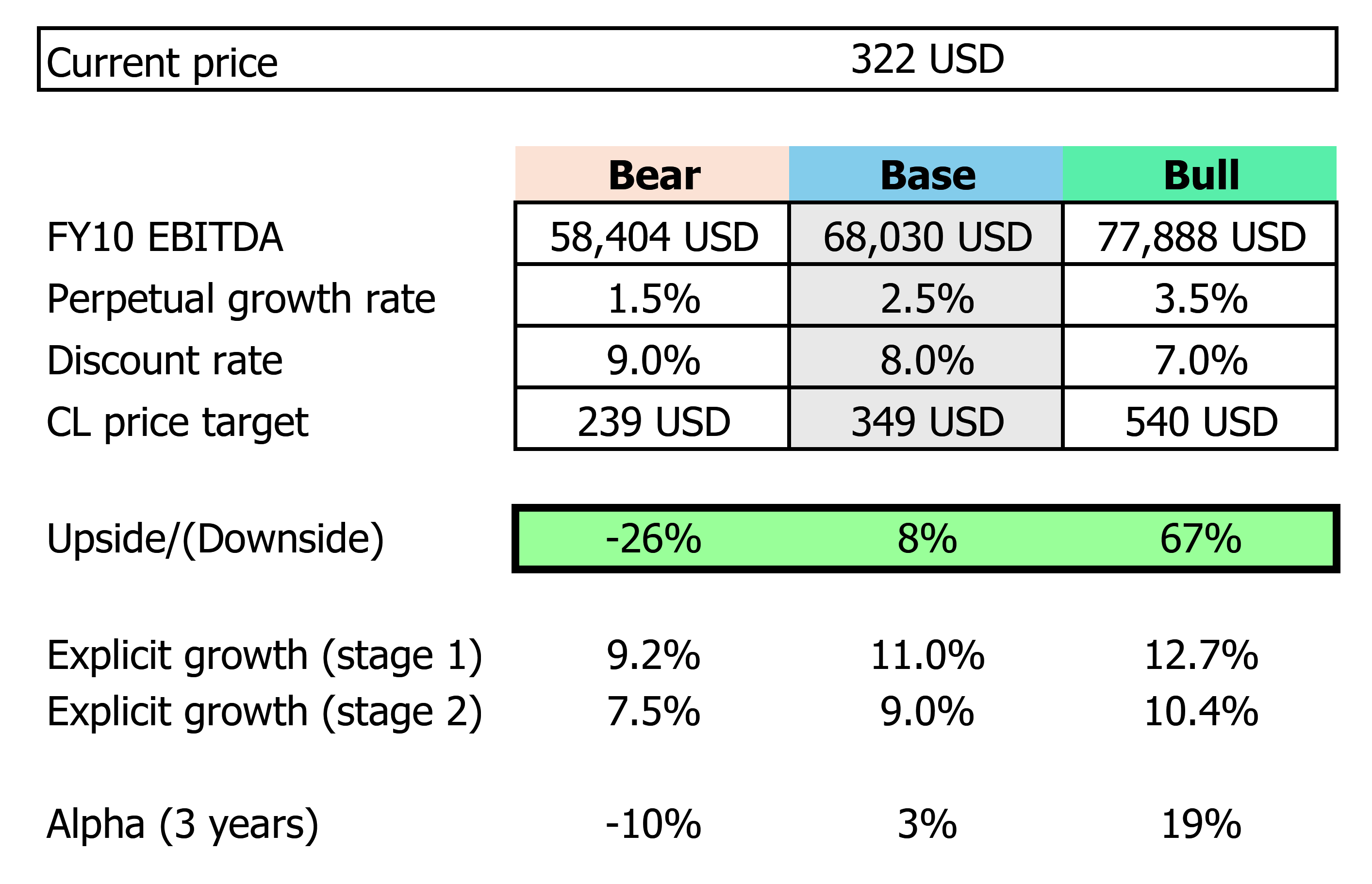

Valuation

DCF Model

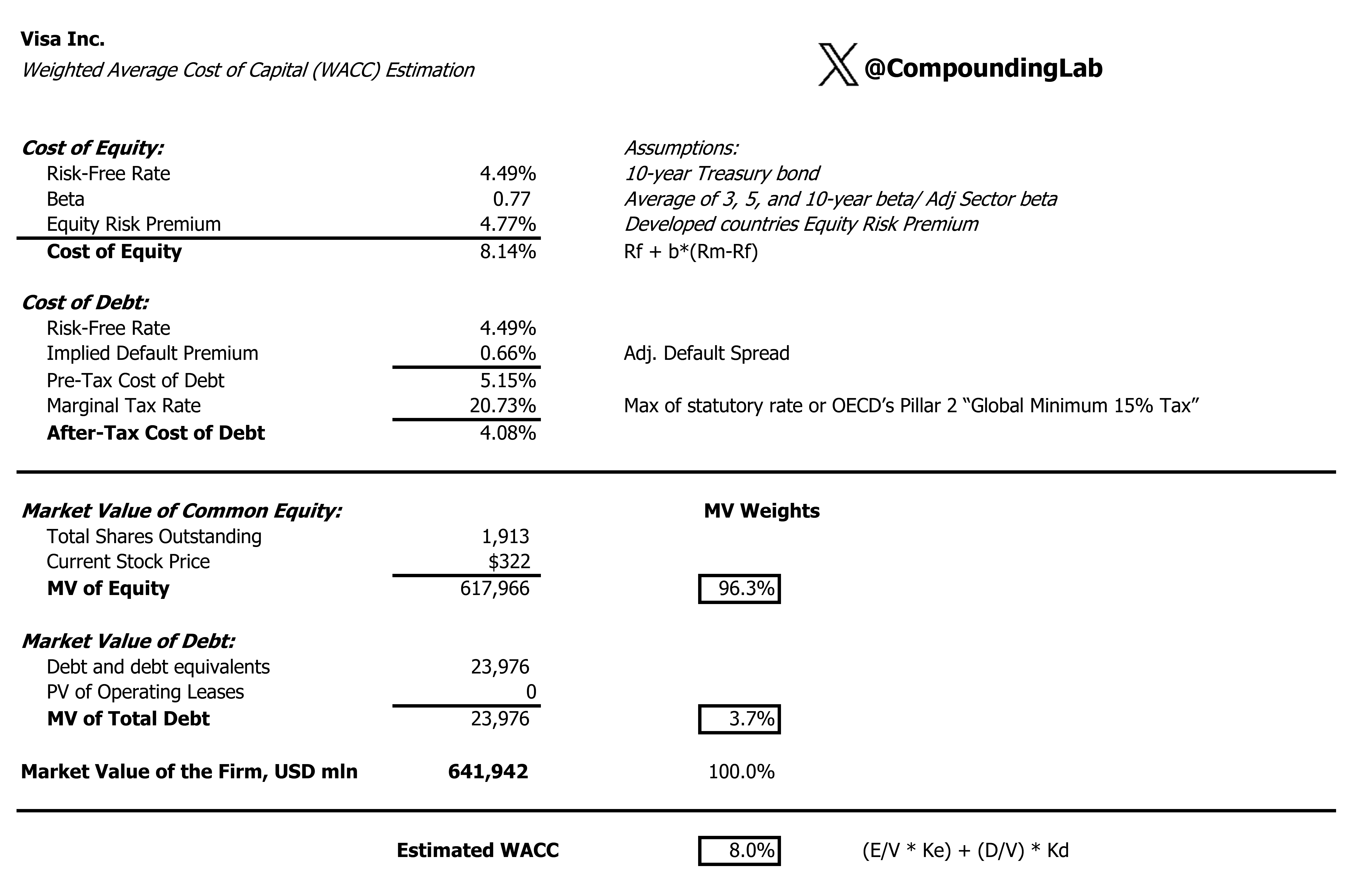

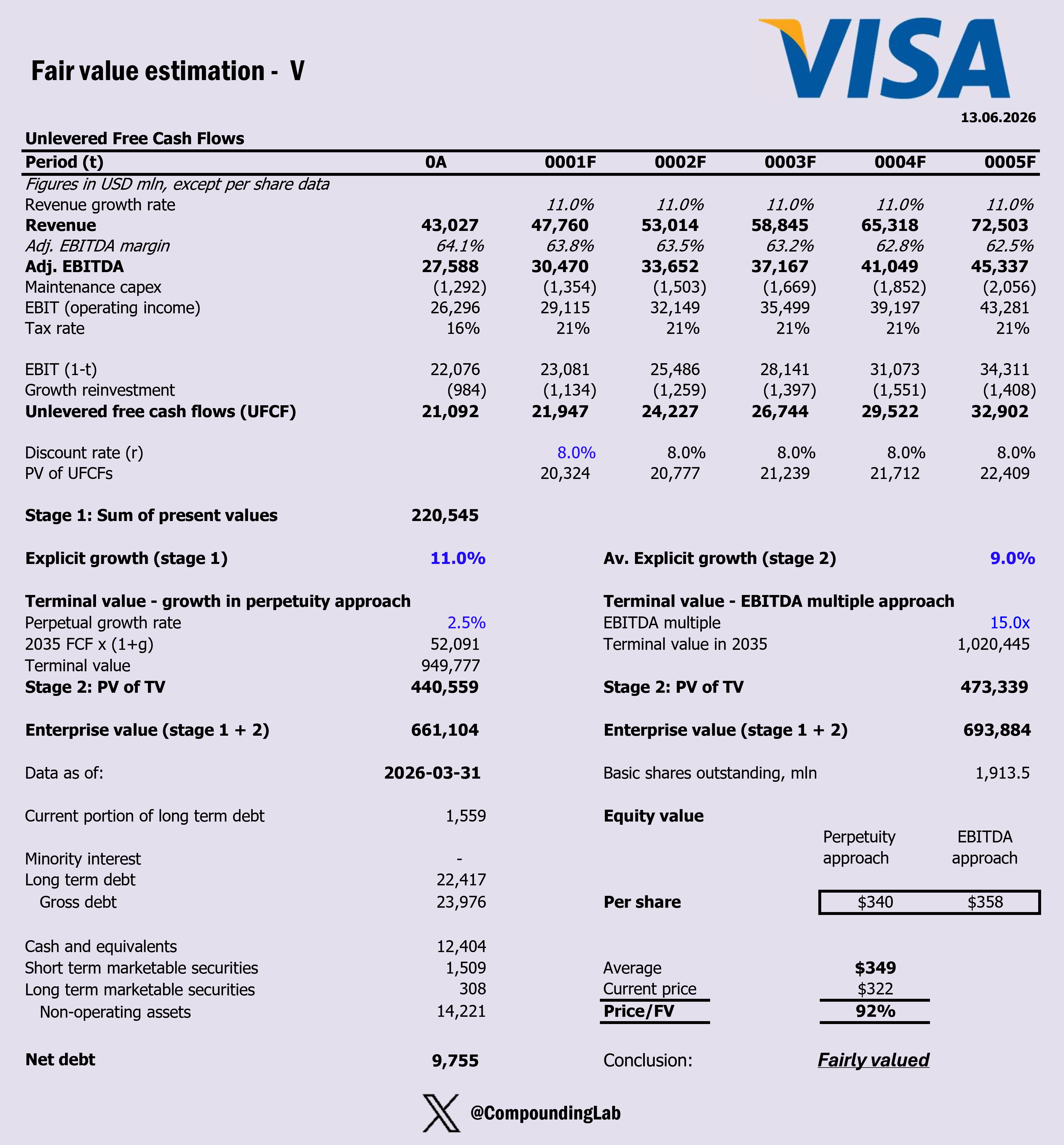

My WACC is 8%, built from a risk-free rate of 4.53% (10-year Treasury), a beta of 0.77 (consistent with Visa’s low cyclicality), an equity risk premium of 4.77%, and an after-tax cost of debt of 3.85%. I use a 2.50% continuing value growth rate, derived by weighting regional GDP expectations with Visa’s spending mix.

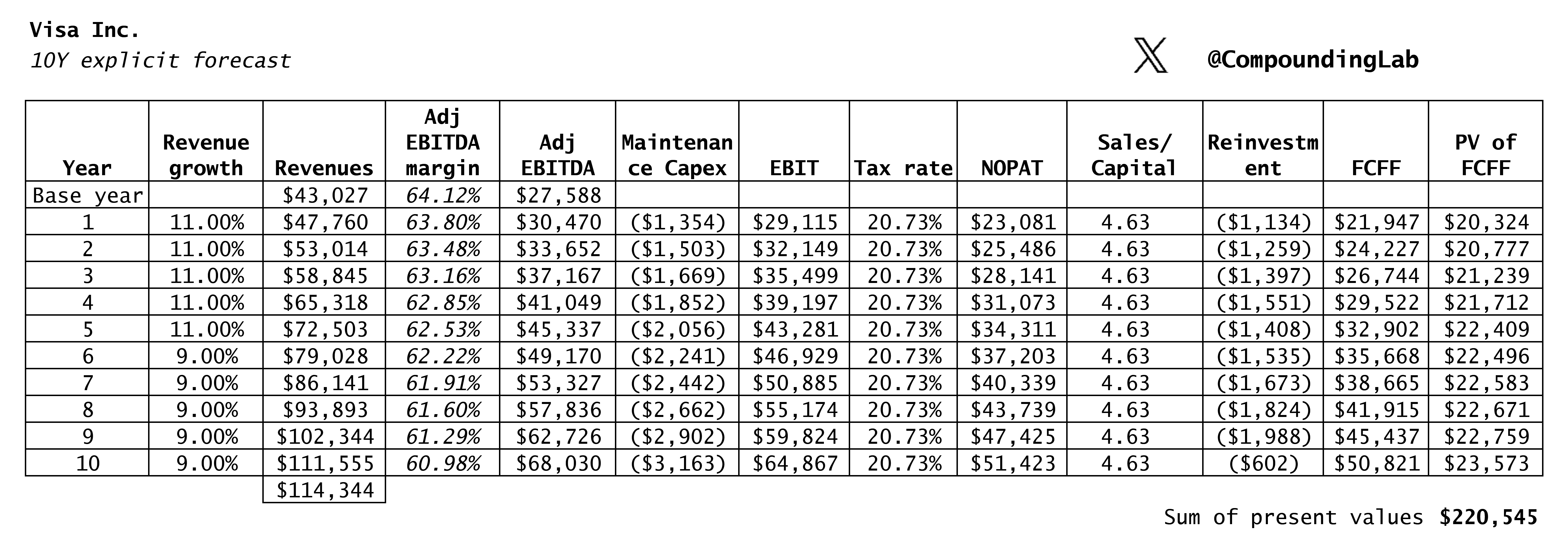

I project FCF growing from $21B in FY2026 to $50B by FY2035. Discounting these cash flows at the WACC produces an operating asset value of $661B, which is a total of sum of explicit present values ($220,545M) and Terminal value ($440,559M or 67%).

After adjusting for excess cash, investment securities, and net debt, the implied equity value calculated using perpetuity approach is $652B, or $340 per share. I then calculate equity value using EBITDA approach, factoring 15x exit multiple in Year 10. This gives me $358 value per share. My target price, based on averaging these two approaches, is $349, which is roughly 8% higher than today’s price.

Dividend Discount Model

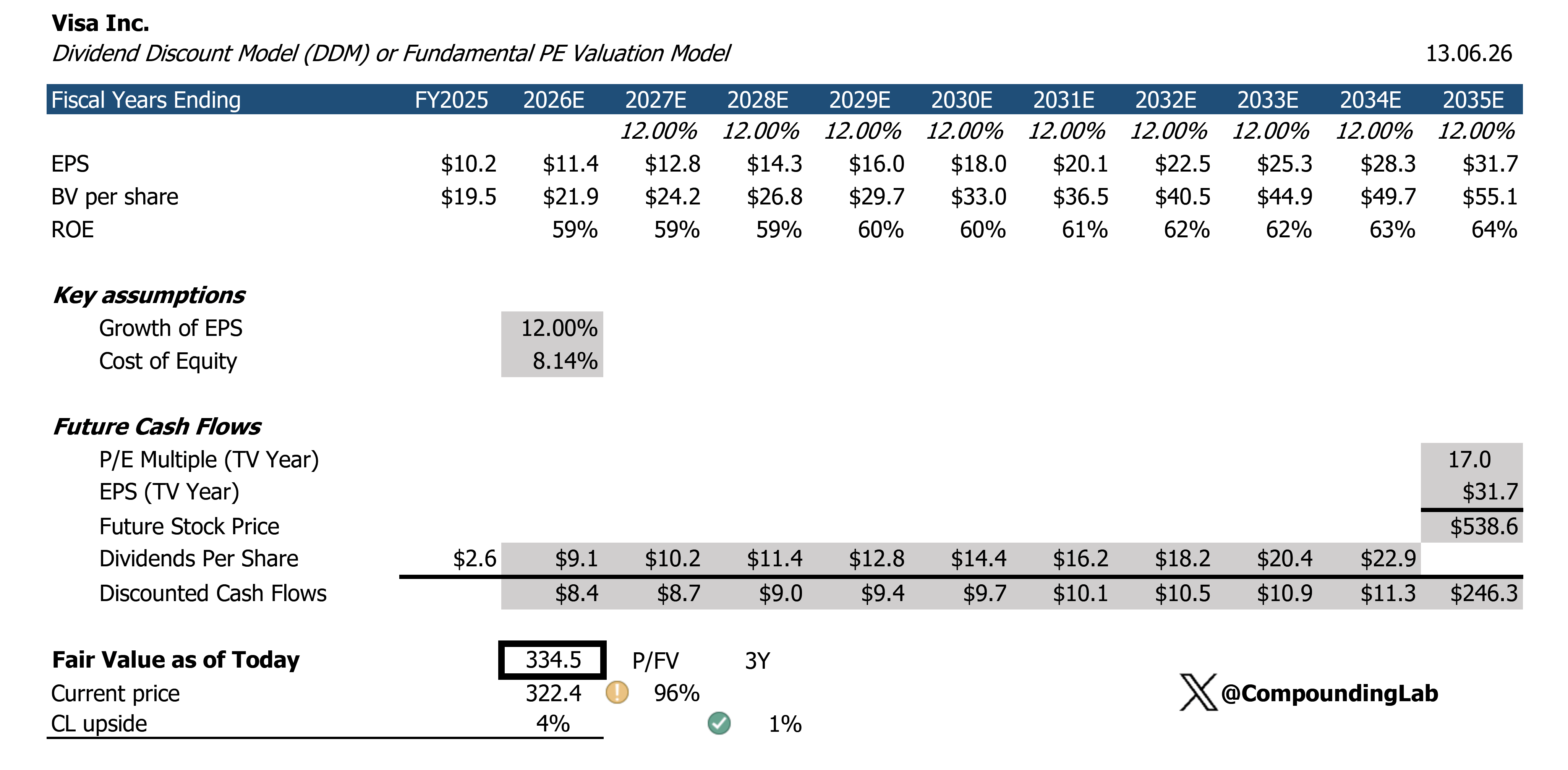

I run a DDM as a secondary cross-check. Using a terminal P/E of 17x on FY2035 EPS of $31.70, the implied future price is $538. Discounted alongside the dividend stream at an 8.11% cost of equity, this gives an intrinsic value of $334 today. The DDM gives a lower value than my DCF, which makes sense: Visa returns most of its capital through buybacks rather than dividends, and the DDM underestimates total shareholder returns. I treat it as a floor estimate.

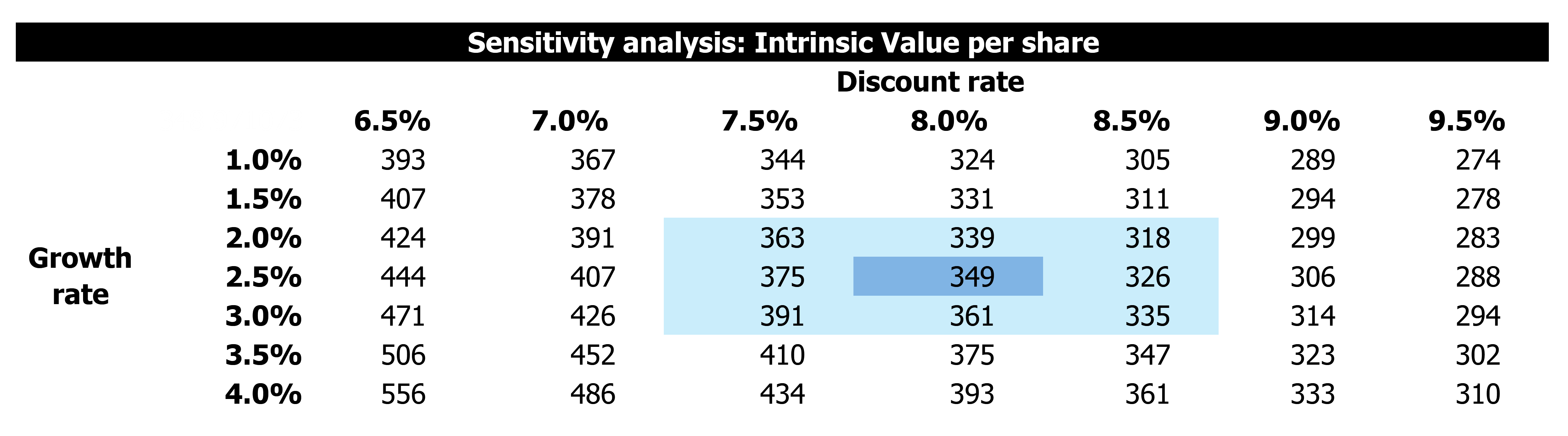

Sensitivity

As always, for prudency purposes I am sharing sensitivity workings, where you can choose your own assumptions based on the tables below.

Feel free to share this article by pressing the button below so that more people can see it.

Key Risks to Monitor

1. The Credit Card Competition Act

This is the single greatest regulatory risk to the investment thesis, and I won’t minimize it. The CCCA, if passed, would require large credit card issuers to enable routing over at least two unaffiliated networks - directly attacking Visa’s ability to lock in exclusive routing relationships and command premium take rates.

The bill has failed to pass in prior legislative sessions, but the underlying political logic — reducing swipe-fee costs for merchants and, at least in theory, consumers — has bipartisan appeal and is unlikely to disappear. The important risk is not mere reintroduction, which has already happened, but evidence of real legislative traction: committee markup or advancement, attachment to a must-pass bill, support from congressional leadership, or a meaningful shift in the vote count. Any of those would be a clear threshold event requiring reassessment of the thesis.

2. Alternative Payment Rails

A2A payment systems, real-time payment networks, and stablecoins are the longer-term competitive threat. In certain markets - Brazil, India, parts of Europe - A2A payments already handle a meaningful share of point-of-sale volume. I would track three key indicators here: A2A penetration in the U.S. surpassing 10%, meaningful merchant adoption of low-cost routing tools, and stablecoin volumes exceeding 2-3% of global payment flows.

3. Cybersecurity and Fraud

Rising payment fraud is simultaneously a risk and a tailwind for Visa. On the risk side, high fraud rates create friction in the system and raise issuer costs. On the tailwind side, it’s a direct driver of demand for Visa’s fraud-prevention and tokenization VAS, which have been growing at 20%+ annually. The key metric to watch: whether global fraud losses grow materially faster than transaction volume, suggesting Visa’s tools are falling behind the threat environment.

Bottom Line

Visa is a classic quality compounder: high margin, high return on invested capital, asset-light, globally scaled, and deeply embedded in commerce. The stock is not priced for disaster, but the valuation is still reasonable if the company continues to compound revenue and free cash flow while expanding value-added services.

My base-case fair value is $349. That gives roughly 8% upside, supported by a DCF/EBITDA value of $358 and partially offset by a more conservative DCF/perpetuity valuation. I would not underwrite big multiple expansion here. The upside has to come mostly from earnings growth, cash generation, and continued buybacks.

My view: Visa remains a Buy for long-term investors who want quality and durability rather than maximum upside. The main reason to own it is not that the stock is optically cheap. The reason is that the business remains one of the strongest toll roads in global payments, and the move toward digital commerce still has a long runway.

Disclosure & Disclaimer

This article is written for informational and educational purposes only and does not constitute investment advice or a solicitation to buy or sell any security. The author may hold positions in securities mentioned. All figures are based on publicly available sources including Visa’s 10-K filings, CapIQ, and the author’s own financial models. Estimates involve judgment and are subject to error. Past performance does not guarantee future results. Please conduct your own due diligence before making any investment decisions.