$XYZ

Block Inc provides payment services to merchants through two segments: Square and Cash App.

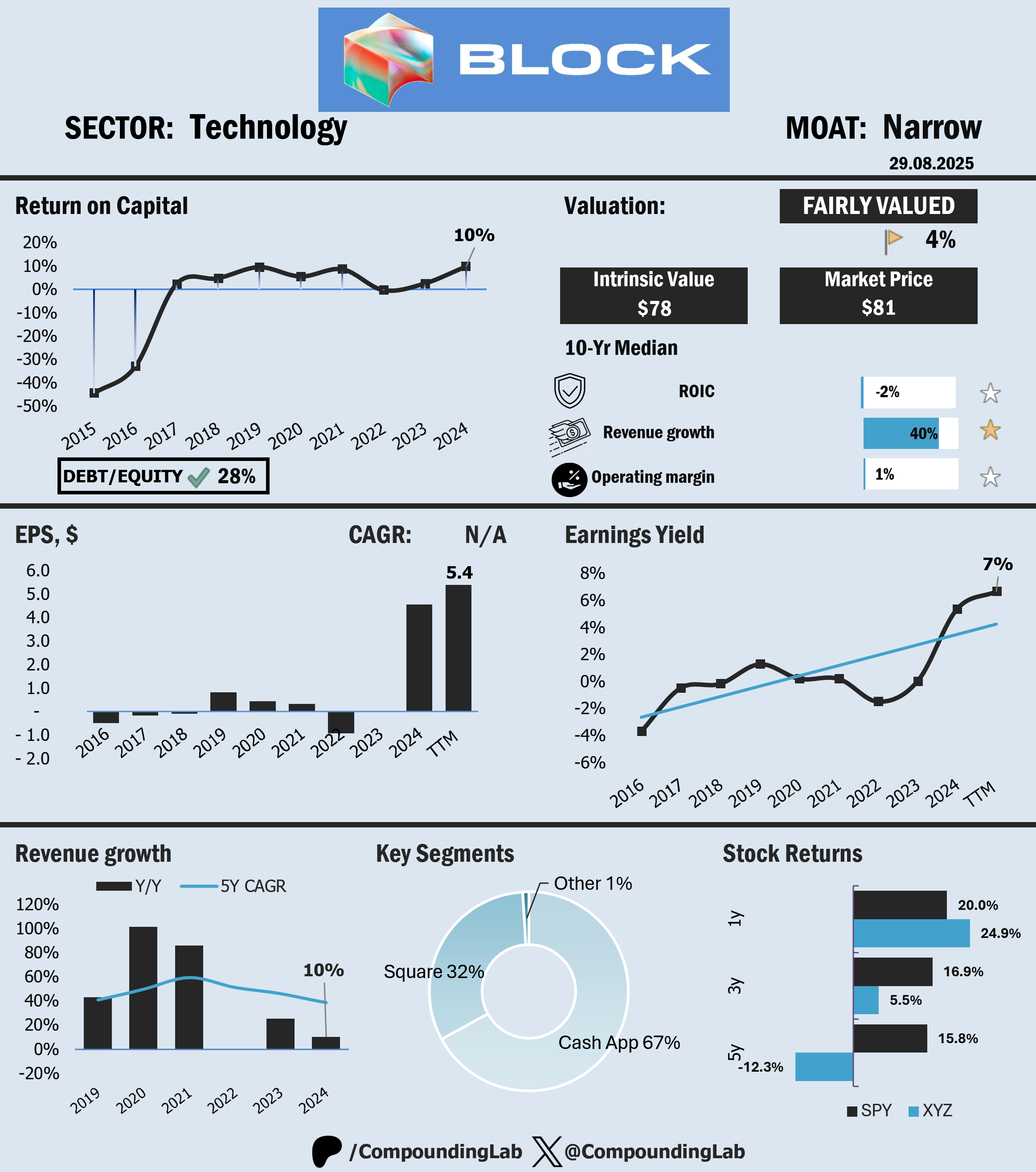

Company only recently started generating decent net income and we can see that this resulted in growth in earnings yield, which is now 7%. But here is significant income charge included ($1.5 bln), which we need to reverse since it's a one-off item. Thus, actual yield will be much less at around 3%.

What is attractive from the data we see on the chart, is very high growth rate. 40% CAGR revenue growth over the past decade is the result of a combination of strategic bets (Cash App), ecosystem expansion (Square seller ecosystem scaling with SMB digitization), and timing. Bitcoin revenue and M&A moves also contributed.

ROIC has been moving into positive territory over the last few years, and I believe management needs to concentrate more on further improving ROIC. There is room for improvement to reach industry level, which is higher than Block's ROIC.

At the moment it is fairly valued, thus I don't expect any meaningful alpha going forward and will not consider it for my portfolio.